Save Big on Commissions ($0.65 per Contract)

CLICK HERE TO LEARN MORE

Save Big on Commissions ($0.65 per Contract)

CLICK HERE TO LEARN MORE

With oil volatility, Iran headlines, major earnings, and fresh consumer data all colliding this week, investors are about to find out whether this move has real strength behind it—or whether another sharp reversal is waiting just beneath the surface.

The market is starting this week in a familiar place: trying to push higher while still absorbing a macro backdrop that remains anything but stable. That tension has defined much of 2026, and it is still the right way to think about this tape now. Investors want to believe the latest rebound can hold, earnings expectations remain supportive, and the broader indexes are not far from record territory. But under the surface, this is still a market being pulled around by geopolitics, oil, interest-rate sensitivity, and rapidly shifting expectations about growth.

The biggest pressure point remains the same: the Strait of Hormuz. Shipping disruptions, renewed tension between the U.S. and Iran, and constant headline swings continue to dominate sentiment across global markets. Even when the market catches a brief break, it does not take much for fear to re-enter the picture. That is because this is not just a geopolitical story. It is an inflation story, a rates story, and a corporate-margin story all at once.

Oil remains at the center of that tension. Prices cratered after Iran temporarily reopened the Strait, helping equities push back toward record territory. But the broader message has not changed. Oil is still highly reactive to every new development, and that means investors cannot get too comfortable. When crude moves sharply, the market immediately has to reassess inflation risk, Federal Reserve expectations, and whether this rally is built on something durable or just another round of relief.

That helps explain the kind of whipsaw action we have seen repeatedly. This is still a market trading headlines first and fundamentals second. Investors are eager to buy any sign of de-escalation, but that bullish response also reveals how fragile conviction still is. The rally has not been driven by a clean reset in the macro backdrop. It has been driven by the hope that the worst-case outcome can still be avoided.

That is what makes this week’s earnings so important. Strong results can help support equities near current levels, but simple beats may not be enough. The market now needs more than backward-looking strength. It needs confidence in forward guidance. It needs signs that demand remains intact, margins can hold up, and corporate leadership teams are not seeing a meaningful deterioration beneath the surface.

Tesla stands out as one of the biggest reports of the week. Its earnings will matter far beyond the EV space. This is the kind of stock that can influence broader appetite for risk, momentum, and high-beta growth. If Tesla delivers a strong report and the market likes the tone, it could reinforce the idea that investors are still willing to reward innovation and future-facing growth stories even in a noisy macro environment. If it disappoints, that could quickly put pressure back on the areas of the market that have helped lead sentiment.

Other major names on deck matter as well. GE Vernova offers an important read into the infrastructure side of the AI story, especially as investors continue to focus on electricity demand, power generation, and the real-world buildout needed to support the next phase of artificial intelligence. Intel will be closely watched for what it says about semiconductor momentum and the durability of the chip trade. Netflix will give investors another look at the resilience of subscription spending and the broader consumer. Even airline earnings from Alaska Air and United Airlines have added significance this week because they offer insight into travel demand and fuel-cost pressure at the same time.

Beyond earnings, the macro calendar is packed with catalysts that could shape the market’s next move. Retail sales will be one of the most important data points because they speak directly to the health of the U.S. consumer. If spending remains firm, that supports the idea that the economy is still holding together despite the pressure from inflation, rates, and geopolitical stress. If spending weakens, recession concerns could move back to the forefront quickly.

Consumer sentiment will matter for a similar reason. If confidence remains historically soft, it reinforces the idea that households are still feeling squeezed, even if equity markets are acting resilient. That disconnect matters. A market can ignore macro discomfort for a while, but it becomes much harder to do so if consumer weakness starts showing up more clearly in spending patterns and corporate commentary.

Fed Chair-designate Kevin Warsh’s testimony is another key event this week. Leadership expectations around the Federal Reserve always matter, but they matter even more in an environment where investors are already trying to figure out how oil, inflation, and growth risks interact. If the market senses a more hawkish tone, rate-sensitive areas could come under renewed pressure. If investors hear something more balanced, that could help steady the tape, at least temporarily.

Gold’s strength also fits the broader picture. Investors may still be willing to buy equities, but the bid for safe havens shows that caution has not disappeared. That combination tells you a lot about the current environment. This is not a market built on total confidence. It is a market balancing optimism with protection, upside participation with defensive hedging.

That is why I remain in the market-neutral camp. The bullish case is not hard to see. Stocks are hovering near highs, earnings expectations remain healthy, and investors continue to reward quality when uncertainty cools even briefly. But the fragile case is just as real. Oil sensitivity remains high. Inflation pressure could return quickly if energy markets tighten again. Interest-rate volatility has not disappeared. And recession concerns are still lurking beneath the surface, especially if consumer or labor data begins to soften more meaningfully.

To me, this still looks like a stock picker’s market. It is not a market that rewards complacency or blind chasing. It rewards selectivity, patience, and disciplined risk management. Investors need to validate trade ideas through both macro and company-specific conditions. They need to understand where leadership is real, where sentiment has simply become too hopeful, and where volatility can still create sudden downside.

The message this week is simple: do not confuse resilience with stability. The market has shown it can withstand fear and keep grinding higher, but it has also shown how quickly that confidence can wobble when oil spikes, geopolitical headlines worsen, or macro data comes in weaker than expected. If earnings hold up, oil stays under control, and the consumer proves more durable than feared, this rally can continue. But if even one of those pillars starts to crack, the next reversal could come fast.

This is still a market that rewards smart defense just as much as offense. And in an environment like this, that balance matters more than ever.

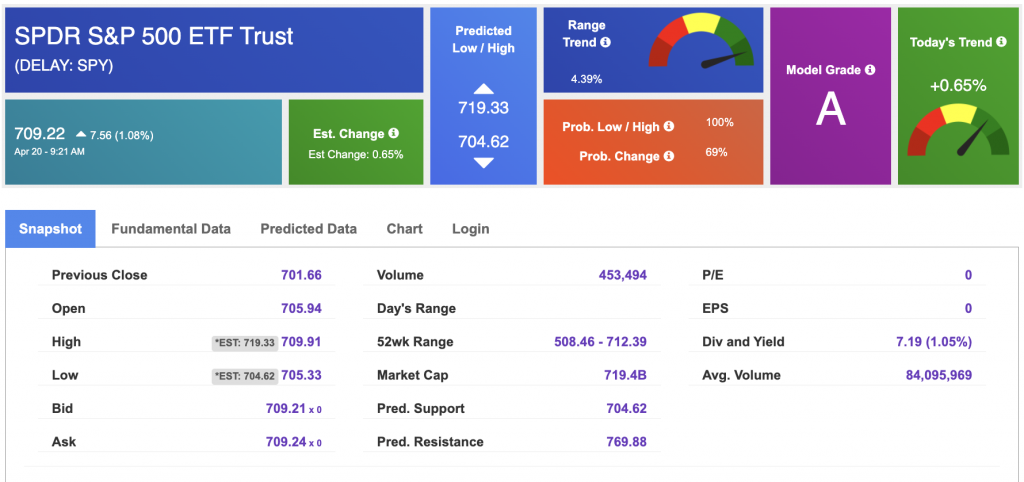

Using the “SPY” symbol to analyze the S&P 500, our 10-day prediction window shows a near-term positive outlook. Prediction data is uploaded after the market closes at 6 p.m. CST. Today’s data is based on market signals from the previous trading session.

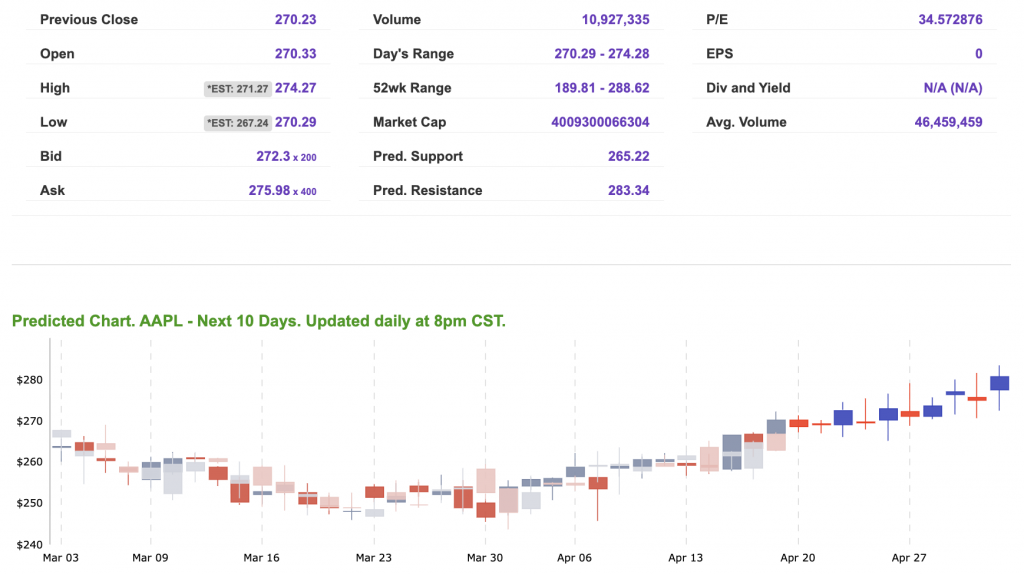

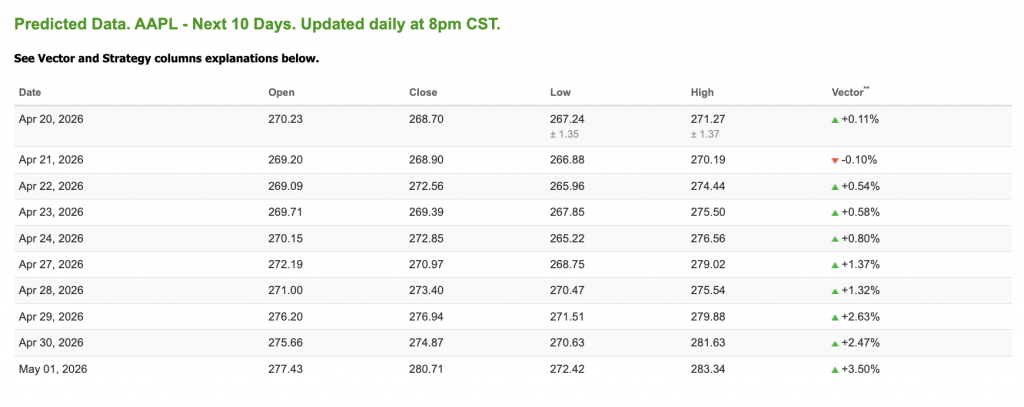

Our featured symbol for Tuesday is AAPL. Apple Inc. (AAPL) is showing a steady vector in our Stock Forecast Toolbox’s 10-day forecast.

The symbol is trading at $272.78 with a vector of +0.11% at the time of publication.

10-Day Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Note: The Vector column calculates the change of the Forecasted Average Price for the next trading session relative to the average of actual prices for the last trading session. The column shows the expected average price movement “Up or Down”, in percent. Trend traders should trade along the predicted direction of the Vector. The higher the value of the Vector the higher its momentum.

*Please note: At the time of publication, Vlad Karpel does have a position in the featured symbol, aapl. Our featured symbol is part of your free subscription service. It is not included in any paid Tradespoon subscription service. Vlad Karpel only trades his money in paid subscription services. If you are a paid subscriber, please review your Premium Member Picks, ActiveTrader, or MonthlyTrader recommendations. If you are interested in receiving Vlad’s picks, please click here.

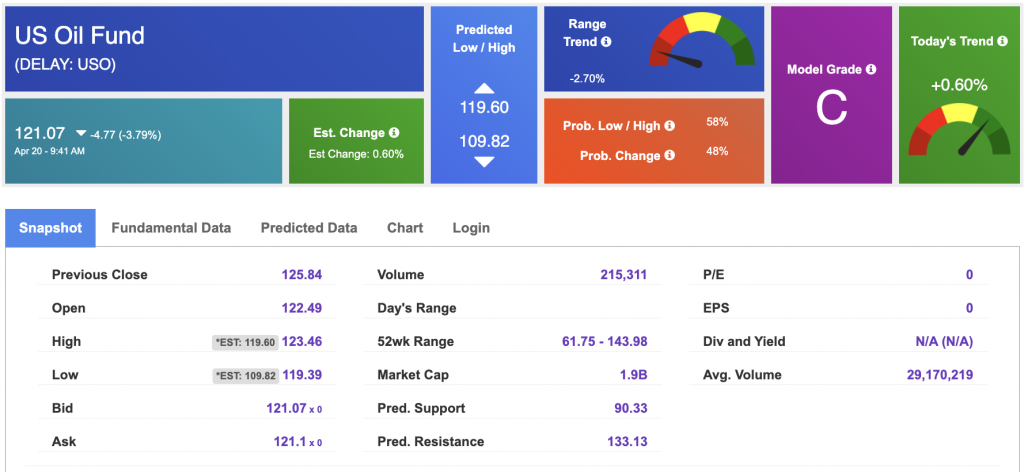

West Texas Intermediate for Crude Oil delivery (CL.1) is priced at $88.31per barrel, up 5.31%, at the time of publication.

Looking at USO, a crude oil tracker, our 10-day prediction model shows mixed signals. The fund is trading at $121.07 at the time of publication. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

The price for the Gold Continuous Contract (GC00) is down 0.98% at $4,831.40 at the time of publication.

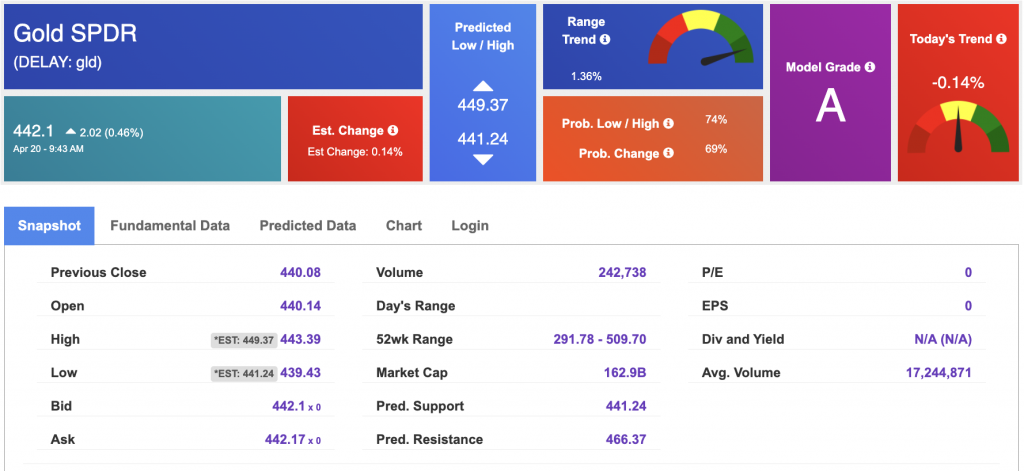

Using SPDR GOLD TRUST (GLD) as a tracker in our Stock Forecast Tool, the 10-day prediction window shows mixed signals. The gold proxy is trading at $442.1 at the time of publication. Vector signals show -0.14% for today. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

The yield on the 10-year Treasury note is down at 4.270% at the time of publication.

The yield on the 30-year Treasury note is down at 4.902 at the time of publication.

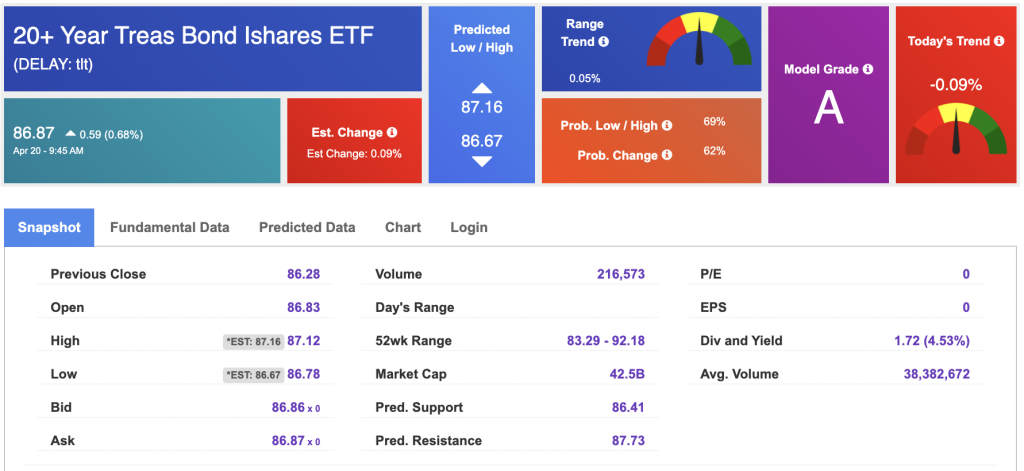

Using the iShares 20+ Year Treasury Bond ETF (TLT) as a proxy for bond prices in our Stock Forecast Tool, we see mixed signals in our 10-day prediction window. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

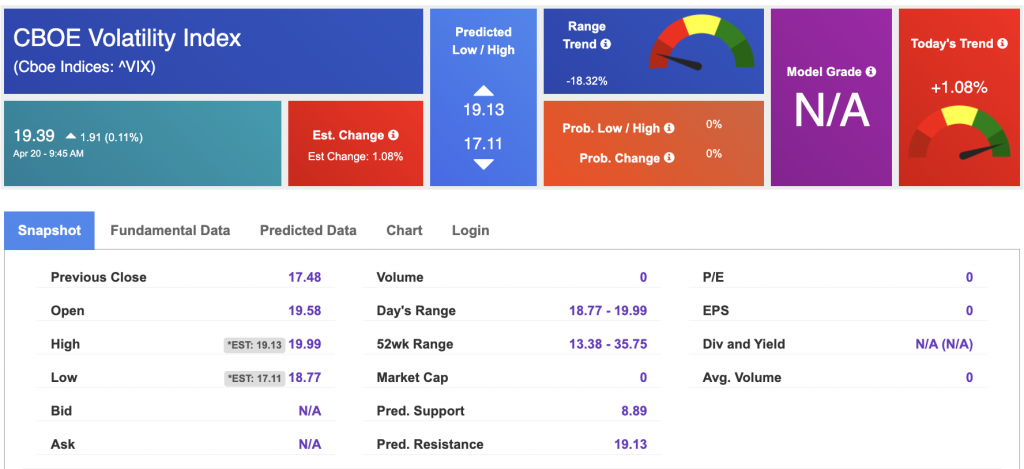

The CBOE Volatility Index (^VIX) is priced at $19.39 at the time of publication, and our 10-day prediction window shows mixed signals. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!