Are you a Long-Term Trader? Then take a look at our NEW RoboInvestor Service?

CLICK HERE TO LEARN MORE

Are you a Long-Term Trader? Then take a look at our NEW RoboInvestor Service?

CLICK HERE TO LEARN MORE

Stocks are pushing deeper into record territory, powered by mega-cap tech, AI optimism, strong earnings, and easing geopolitical fears. But with oil still elevated, the Fed meeting ahead, PCE inflation on deck, and market leadership concentrated in a narrow group of names, this rally now faces an important test. The bulls are in control, but discipline matters more than ever.

Markets are entering the new week with momentum still on their side, but the key question for investors is becoming more important: is this rally broadening into a healthier advance, or is it still being carried by a small group of mega-cap technology and AI-linked leaders?

Last week, stocks closed with another powerful move into record territory. The S&P 500 broke above 7,100 for the first time, while the Nasdaq also reached fresh all-time highs. That price action shows how much confidence has returned after weeks of pressure from geopolitical headlines, oil volatility, tariff concerns, and uncertainty around interest rates. With the VIX near 18, volatility remains contained, but not absent. Investors are willing to take risk again, yet this is still not a market where discipline can be ignored.

The biggest driver behind last week’s strength was geopolitical relief. After weeks of concern tied to the U.S.-Iran conflict and the Strait of Hormuz, markets responded positively to signs that the worst-case scenario may be avoided. Mediators continued working toward extending the fragile ceasefire, President Trump signaled progress in talks, and Iran temporarily reopened the Strait of Hormuz. That helped oil prices cool from their most extreme levels, reduced near-term inflation anxiety, and allowed investors to rotate back into risk assets.

That oil move mattered because crude has been one of the most important swing factors for this market. When energy prices surge, investors have to worry about renewed inflation pressure, weaker consumer spending, margin compression, and a more complicated Federal Reserve path. When oil stabilizes or pulls back, those pressures ease. That was a major reason growth stocks regained traction last week.

But the risk has not disappeared. As we begin this week, oil remains firm again due to ongoing Middle East instability and supply-risk concerns. Energy stocks may benefit from elevated crude, but the broader market does not want to see oil climb in a way that revives inflation fears or forces the Fed to stay restrictive for longer.

Treasury yields are another key part of the story. After last week’s spike, yields have eased slightly, giving some relief to rate-sensitive sectors and high-growth stocks. Markets are still pricing in fewer rate cuts this year, but the tone has stabilized enough to reduce immediate pressure on equities. That has helped large-cap technology regain leadership, especially in AI-linked names and semiconductors.

Technology remains the engine of this market. Large-cap tech and communication services are pulling the indexes higher, while AI-related stocks remain the strongest pocket of leadership. Semiconductors are extending gains after strong earnings last week and continued optimism around AI infrastructure spending. Intel’s stronger-than-expected report helped spark a rally across the chip space, reinforcing the idea that semiconductor momentum remains intact.

That matters because semiconductors remain one of the most important leadership groups in the entire market. When chips are strong, they often support broader confidence in AI, cloud infrastructure, software, data centers, and mega-cap technology. That helps explain why the Nasdaq continues to outperform and why investors are still willing to pay for companies tied to artificial intelligence, productivity growth, and long-term infrastructure demand.

At the same time, leadership remains narrow. Market breadth is not as strong as the headline indexes suggest. Tech and communication services are doing much of the heavy lifting, while other areas are participating more unevenly. This is why I do not view the current rally as a simple “buy everything” environment. It is still a selective market, and that selectivity matters.

Earnings have helped support the bullish case. Q1 earnings season started on solid footing, led by better-than-expected results from major banks including JPMorgan, Bank of America, Wells Fargo, Morgan Stanley, and Goldman Sachs. Resilient trading activity, investment banking strength, and healthier-than-feared financial conditions helped reinforce the idea that the economy is still holding up despite higher rates and macro pressure.

Outside of mega-cap technology, corporate results have also shown pockets of strength. Masco posted better-than-expected Q1 results, while Steel Dynamics rallied on record shipments and strong pricing. Those reports helped show that parts of the industrial, housing-related, and materials economy remain stronger than expected. This kind of broadening is exactly what bulls want to see if the rally is going to become more durable.

Now the market faces a much bigger test. This week brings the Federal Reserve meeting, a major wave of earnings, PCE inflation, consumer confidence, jobless claims, PMIs, global macro updates, and Treasury auctions. Any one of those events can shift sentiment, but together they create one of the more important weeks of this rally.

The Fed is widely expected to hold rates steady, so the real focus will be on the statement and press conference. Investors will be listening closely for any shift in language around inflation persistence, labor-market cooling, and the timing of the first potential rate cut. If the Fed sounds more patient or more concerned about inflation, yields could move higher again. If the Fed acknowledges cooling without sounding alarmed, equities may find support.

PCE inflation may be even more important. Because PCE is the Fed’s preferred inflation gauge, a hotter-than-expected reading could quickly pressure stocks, especially high-valuation growth names. Consumer confidence, jobless claims, and manufacturing and services PMIs will also help shape the market’s view of the economy. If inflation remains sticky while growth softens, investors may have to reassess the current optimism. If the data holds up, the rally could continue.

Treasury auctions also deserve attention. Demand for mid- and long-duration debt has recently become a source of volatility. Weak auction demand can push yields higher and create pressure across equities. In a market trading near record highs, even small shifts in the rate backdrop can matter.

Global signals are mixed as well. European markets are slightly softer as investors digest earnings and await key inflation data. Asian markets were mixed overnight, with China showing modest strength while Japan pulled back after recent highs. Eurozone inflation data, China manufacturing updates, and ongoing geopolitical developments in the Middle East and Eastern Europe will continue influencing commodities, currencies, and global risk sentiment.

That brings us back to the main point: the market is strong, but it is not risk-free. Record highs are encouraging, but they can also create complacency. The long-term trend remains intact, and the rally can continue if earnings hold up, oil stays contained, yields remain stable, and the Fed avoids surprising investors with a more hawkish tone. But momentum beneath the surface has become more uneven, and leadership remains concentrated.

I remain in the market-neutral camp. I believe the SPY rally can continue toward the $680–$700 range if the current trend holds, with short-term support in the $620–$650 area over the next few months. But this is not a market where investors should chase blindly. Higher-for-longer rates, rising unemployment indicators, oil volatility, and narrow breadth all argue for selectivity.

The next phase of this rally will likely depend on whether mega-cap earnings can justify the move. Investors will be watching Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, Tesla, and other major leaders for updates on AI spending, cloud demand, margins, advertising trends, consumer behavior, and forward guidance. These companies carry enormous weight in the indexes, so their reports could determine whether the rally broadens or becomes more fragile.

For now, the message is clear: the market has regained confidence, but discipline still matters. Tech and AI leadership remain powerful, earnings have been supportive, and volatility is contained. But the Fed, PCE inflation, Treasury yields, oil prices, and geopolitical headlines can still shift sentiment quickly.

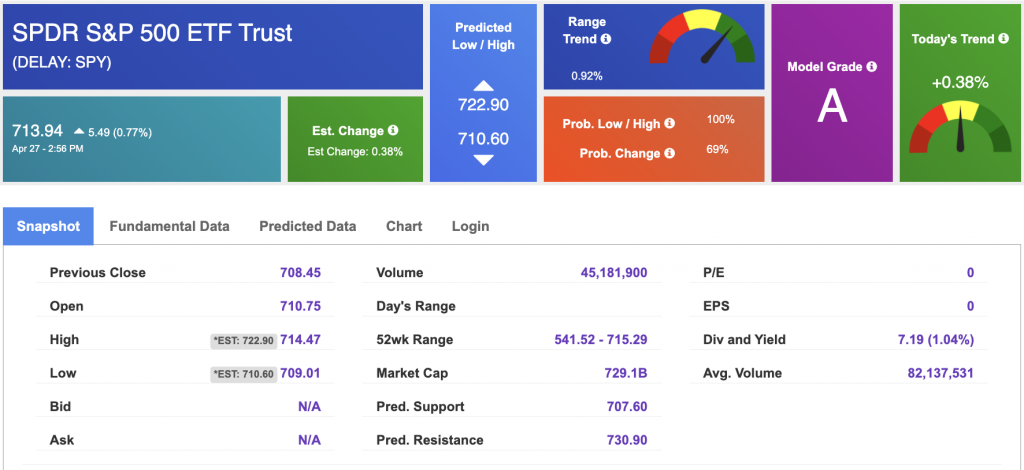

Using the “SPY” symbol to analyze the S&P 500, our 10-day prediction window shows a near-term positive outlook. Prediction data is uploaded after the market closes at 6 p.m. CST. Today’s data is based on market signals from the previous trading session.

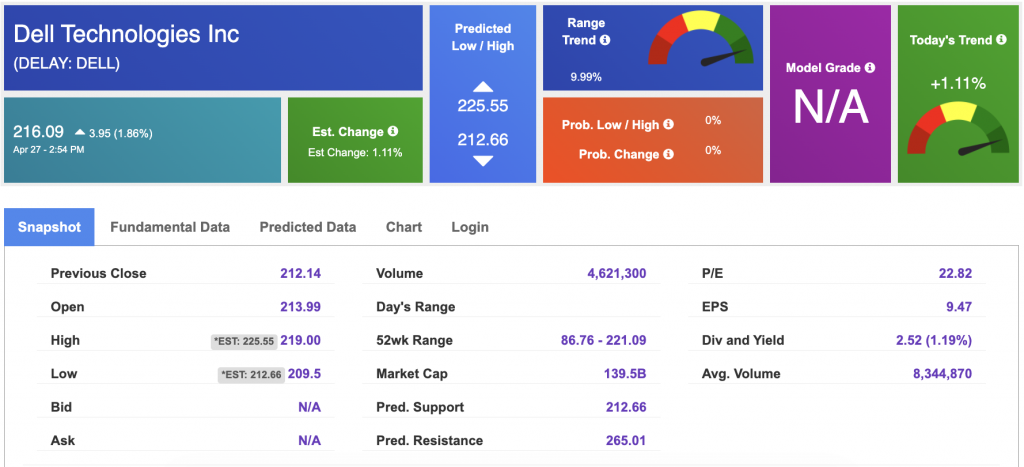

Our featured symbol for Tuesday is DELL. Dell Technologies Inc. (DELL) is showing a steady vector in our Stock Forecast Toolbox’s 10-day forecast.

The symbol is trading at $216.09 with a vector of +1.11% at the time of publication.

10-Day Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Note: The Vector column calculates the change of the Forecasted Average Price for the next trading session relative to the average of actual prices for the last trading session. The column shows the expected average price movement “Up or Down”, in percent. Trend traders should trade along the predicted direction of the Vector. The higher the value of the Vector the higher its momentum.

*Please note: At the time of publication, Vlad Karpel does have a position in the featured symbol, DELL. Our featured symbol is part of your free subscription service. It is not included in any paid Tradespoon subscription service. Vlad Karpel only trades his money in paid subscription services. If you are a paid subscriber, please review your Premium Member Picks, ActiveTrader, or MonthlyTrader recommendations. If you are interested in receiving Vlad’s picks, please click here.

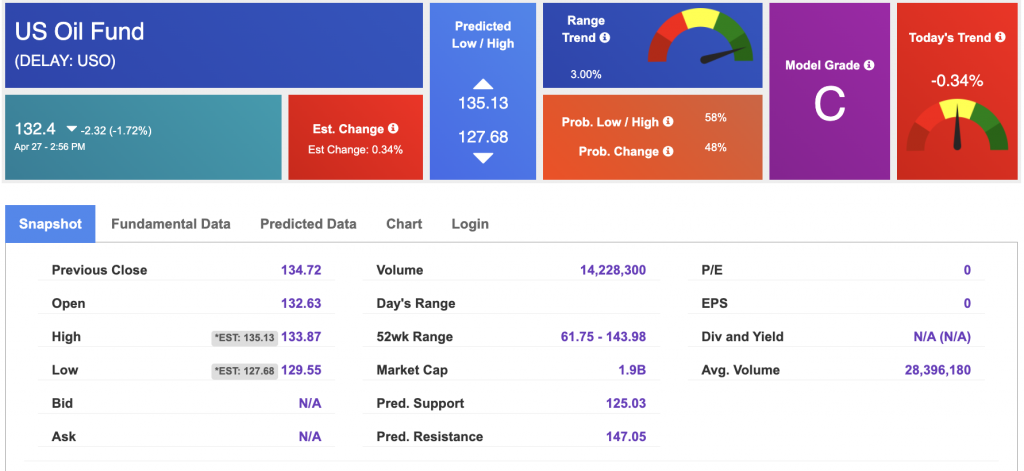

West Texas Intermediate for Crude Oil delivery (CL.1) is priced at $96.32 per barrel, up 2.03%, at the time of publication.

Looking at USO, a crude oil tracker, our 10-day prediction model shows mixed signals. The fund is trading at $132.40 at the time of publication. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

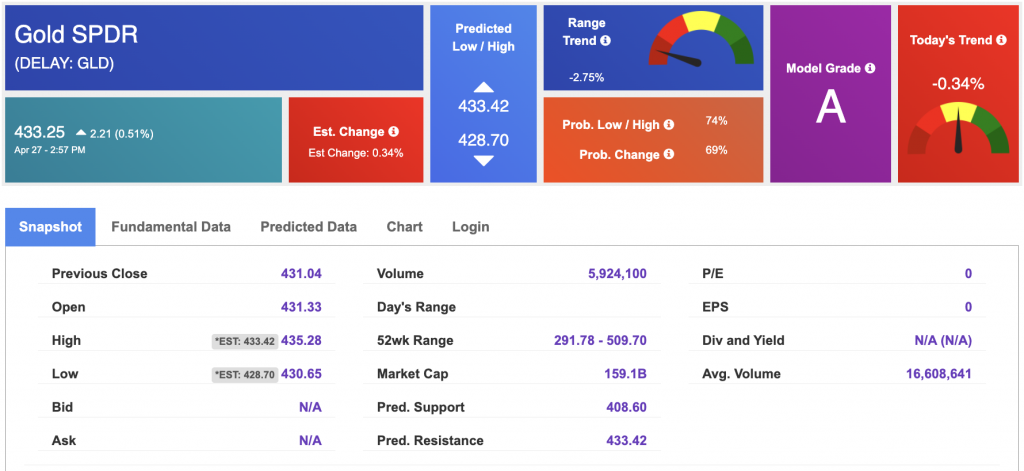

The price for the Gold Continuous Contract (GC00) is down 0.96% at $4,695.50 at the time of publication.

Using SPDR GOLD TRUST (GLD) as a tracker in our Stock Forecast Tool, the 10-day prediction window shows mixed signals. The gold proxy is trading at $433.25 at the time of publication. Vector signals show -0.34% for today. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

The yield on the 10-year Treasury note is up at 4.338% at the time of publication.

The yield on the 30-year Treasury note is up at 4.942 at the time of publication.

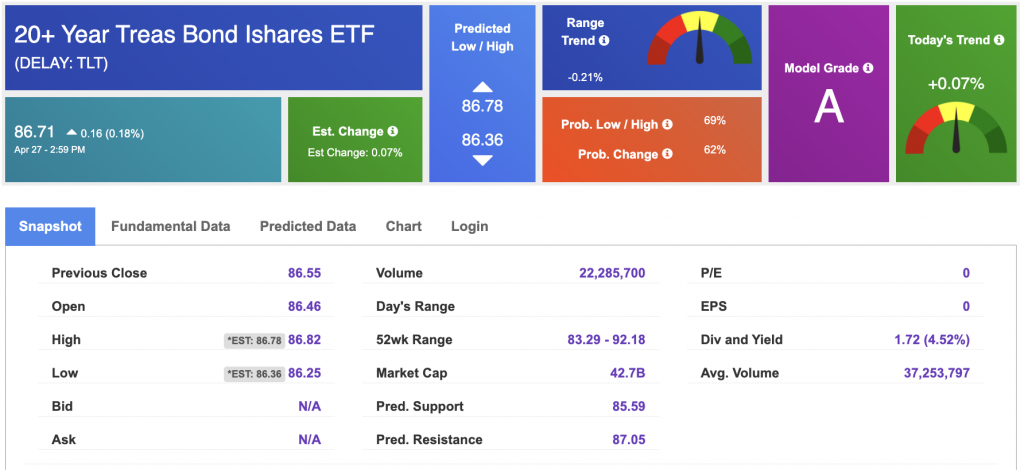

Using the iShares 20+ Year Treasury Bond ETF (TLT) as a proxy for bond prices in our Stock Forecast Tool, we see mixed signals in our 10-day prediction window. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

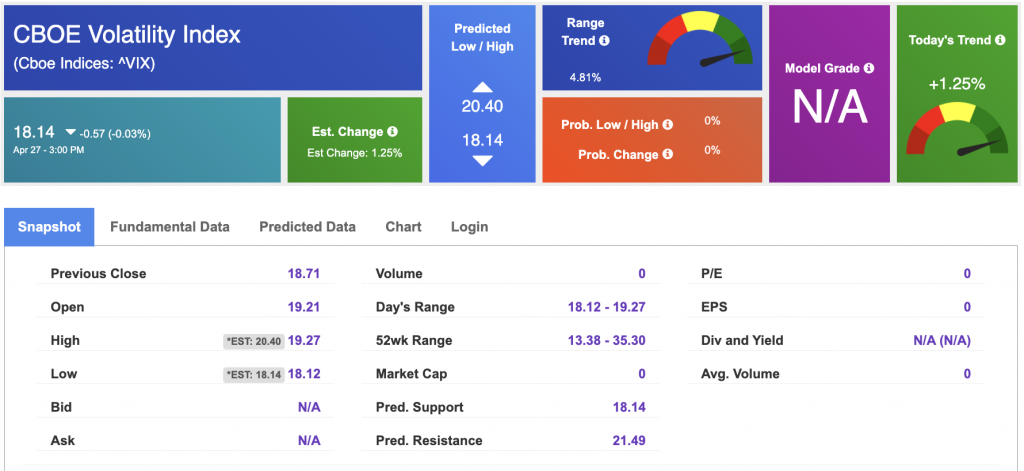

The CBOE Volatility Index (^VIX) is priced at $18.14 at the time of publication, and our 10-day prediction window shows mixed signals. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!