Save Big on Commissions ($0.65 per Contract)

CLICK HERE TO LEARN MORE

Save Big on Commissions ($0.65 per Contract)

CLICK HERE TO LEARN MORE

U.S. stocks are opening June near record highs as AI momentum, stronger manufacturing data, and resilient corporate earnings continue to fuel investor optimism. But with Iran threatening the Strait of Hormuz, oil prices swinging sharply, tariffs still pressuring inflation expectations, and this week’s jobs report set to shape Fed policy expectations, the rally now faces one of its most important tests of the summer.

U.S. stocks are starting the week with momentum still favoring the bulls, but the market is entering June with several important crosscurrents that investors cannot ignore. Major indexes remain at or near record highs, the VIX continues to hover around 17, and buyers are still stepping in on weakness. That combination tells us market sentiment remains constructive. Investors are not operating from a place of fear. Instead, they continue to reward technology leadership, AI-driven growth, resilient earnings, and signs that the economy may still be strong enough to support a soft landing.

At the same time, this is not a risk-free rally. The market is being pulled between two powerful forces. On one side, AI momentum, stronger manufacturing data, improving global demand for chips, and steady corporate earnings continue to support higher stock prices. On the other side, Iran-related oil volatility, tariff uncertainty, sticky inflation risk, volatile Treasury yields, and this week’s major employment data all have the potential to test investor confidence.

The biggest headline today came from the energy market. Crude prices surged after Iran threatened to completely block the Strait of Hormuz, one of the most important shipping routes in the world. That immediately raised concerns about global oil supply, shipping disruptions, and renewed inflation pressure. A sharp move higher in oil matters because it can filter through the economy quickly, affecting gasoline prices, transportation costs, corporate margins, and inflation expectations. Later in the session, however, oil prices eased as hopes improved for a possible extension of the U.S.–Iran truce. That reversal helped calm investors and allowed equities to focus again on technology strength and economic resilience.

The Iran situation remains one of the most important risks for markets right now. If tensions escalate and oil prices remain elevated, inflation expectations could rise again just as investors are hoping the Federal Reserve will have room to cut rates later in the year. If diplomacy improves and oil continues to ease, that would remove one of the market’s biggest near-term threats and could give stocks more room to extend the rally. For now, investors should expect headlines around Iran, the Strait of Hormuz, and broader Middle East tensions to remain market-moving.

Technology and AI stocks continue to be the strongest engines of the market. The AI trade is not just lifting a handful of mega-cap names anymore. It is spreading across semiconductors, memory chips, servers, cloud infrastructure, software, networking, and even parts of the industrial and manufacturing economy. Dell, Snowflake, Ford, and other companies tied to AI-related demand continue to show how broad the theme has become. Nvidia’s latest AI announcements and ongoing demand for AI infrastructure have helped keep the market focused on growth, productivity, and future earnings potential.

That said, investors also need to be careful not to confuse strong momentum with unlimited upside. Some analysts are beginning to warn that parts of the AI rally may be pricing in very aggressive assumptions. That does not mean the trend is over. It does mean valuation discipline matters more at record highs. The strongest AI-linked companies can still lead, but the market may become more selective if earnings guidance, data-center demand, or semiconductor supply-chain updates fail to keep pace with expectations.

Today’s economic data also supported the bullish case. The ISM Manufacturing PMI rose to 54, its strongest reading since 2022. That is an important signal because manufacturing had been one of the weaker parts of the economy during the higher-rate cycle. A move back into stronger expansion territory helps support the soft-landing narrative. It suggests that businesses are still producing, demand has not collapsed, and the industrial side of the economy may be stabilizing.

Construction spending also came in stronger, rising 0.4% in April. That adds another piece of evidence that the economy remains resilient despite higher borrowing costs. Residential construction showed signs of strength, helped by single-family homebuilding, though housing remains sensitive to mortgage rates. The broader takeaway is that economic activity is not breaking down. Growth remains uneven, but it is still present.

That is exactly why this week’s jobs report becomes so important. The market wants a labor report that is strong enough to confirm the economy is healthy, but not so hot that it forces the Fed to stay restrictive for longer. A hotter-than-expected jobs number could push Treasury yields higher and pressure rate-cut expectations. A weaker-than-expected number could raise concerns that unemployment is starting to rise too quickly. The ideal outcome for bulls would be a balanced report: steady job creation, cooling wage pressure, and no sharp deterioration in unemployment.

The 10-year Treasury yield remains one of the key variables beneath the surface. It has been volatile, trading in a wide range between 3.6% and 4.50%. That wide range keeps investors sensitive to every inflation report, Fed comment, and labor-market update. The market still wants to believe rate cuts are possible later in 2026, but the Fed has not given investors a clear green light. Inflation has improved from its peak, but it is not fully solved. At the same time, unemployment indicators are beginning to tick higher. That creates a more complicated policy backdrop.

Tariffs also remain part of the risk equation. Trade policy continues to affect supply chains, input costs, corporate margins, and inflation expectations. If companies can pass along higher costs, consumers may feel pressure. If companies absorb those costs, margins may compress. For now, earnings resilience and AI growth have allowed markets to look past some tariff concerns. But at record highs, any renewed tariff pressure could quickly become a reason for investors to take profits.

Global markets are also sending a constructive signal. Asian equities have been strong, with South Korea’s KOSPI reaching record highs as AI-driven semiconductor demand powers exports. That matters because the AI theme is global. Strong chip demand in Asia reinforces the idea that AI infrastructure spending remains one of the most important economic and market forces in the world. It also supports the case for continued leadership from semiconductors, memory, cloud infrastructure, and advanced hardware.

Corporate headlines remain supportive as well. SpaceX secured a major U.S. Space Force contract, giving aerospace and defense investors another reminder that government spending, space infrastructure, and advanced technology remain important long-term themes. Apotex Health is pursuing a large Toronto IPO, which could help revive interest in Canada’s IPO market. Meanwhile, companies tied to AI demand continue to attract attention across sectors, from hardware and servers to software and industrial applications.

Looking ahead, this week’s watch list is important. Investors will be focused on the employment report, JOLTS job openings, ADP private payrolls, ISM Services, jobless claims, productivity data, and any new inflation signals. These reports will help shape expectations around growth, labor-market strength, wage pressure, and Fed policy. On the earnings side, updates from companies such as HPE, PANW, AVGO, CRWD, CIEN, and IOT will be important for technology, cybersecurity, networking, and AI infrastructure sentiment.

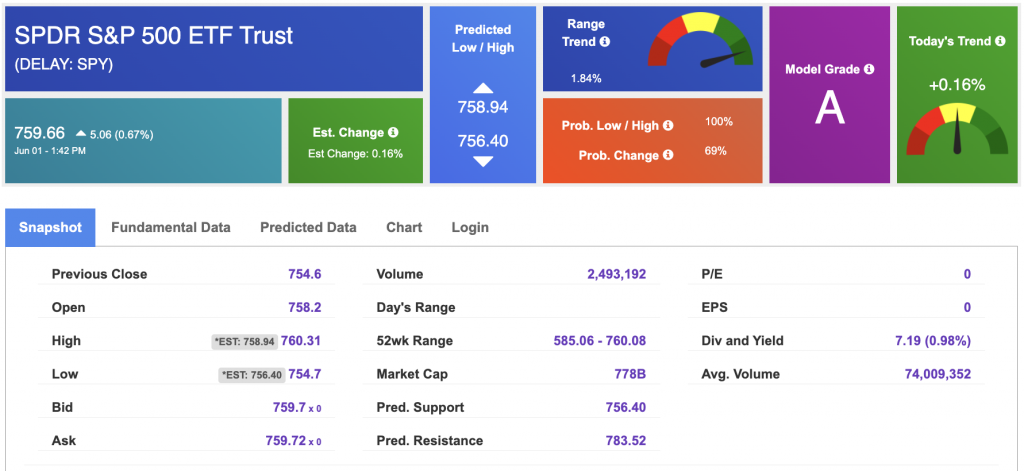

From a market standpoint, I remain in the bullish camp. The long-term trend is intact, and the market continues to behave well despite a difficult headline environment. With the VIX near 17, major indexes trading near all-time highs, and AI leadership still strong, the path of least resistance remains higher. As long as buyers continue defending key support, the SPY rally can still extend toward the $740–$760 area. Short-term support remains in the $680–$700 range over the next few months.

But bullish does not mean careless. At all-time highs, the market becomes more vulnerable to sharp pullbacks if oil spikes, yields rise, inflation surprises higher, unemployment weakens faster than expected, or geopolitical headlines deteriorate. This is a market where momentum favors the bulls, but discipline remains essential. Investors should continue to participate in strength, but avoid chasing extended moves without a plan.

The main message for this week is simple: the rally is still alive, but it now needs confirmation. AI leadership, improving manufacturing data, resilient construction spending, and global chip demand all support the bullish case. But the jobs report, oil volatility, Fed expectations, tariffs, and Middle East headlines will determine whether the market can keep climbing or needs to pause and reset.

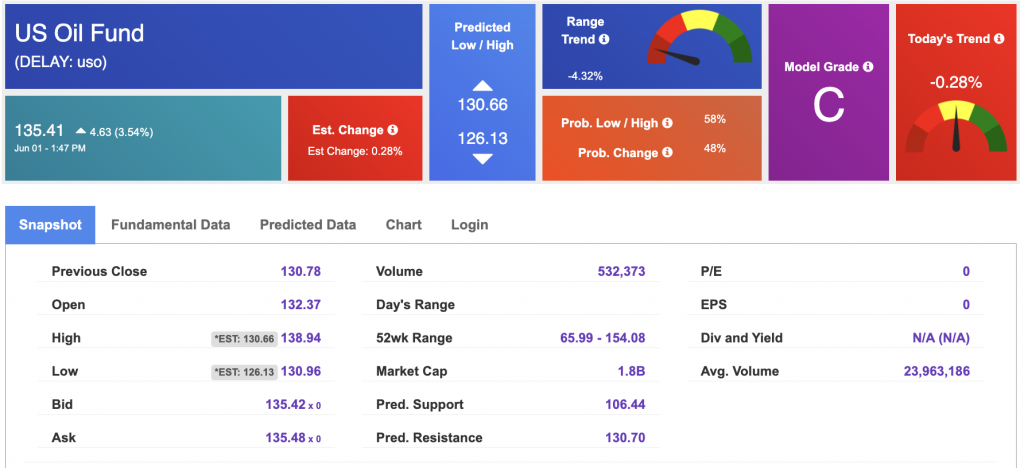

West Texas Intermediate for Crude Oil delivery (CL.1) is priced at $92.63per barrel, up 6.00%, at the time of publication.

Looking at USO, a crude oil tracker, our 10-day prediction model shows mixed signals. The fund is trading at $135.41 at the time of publication. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

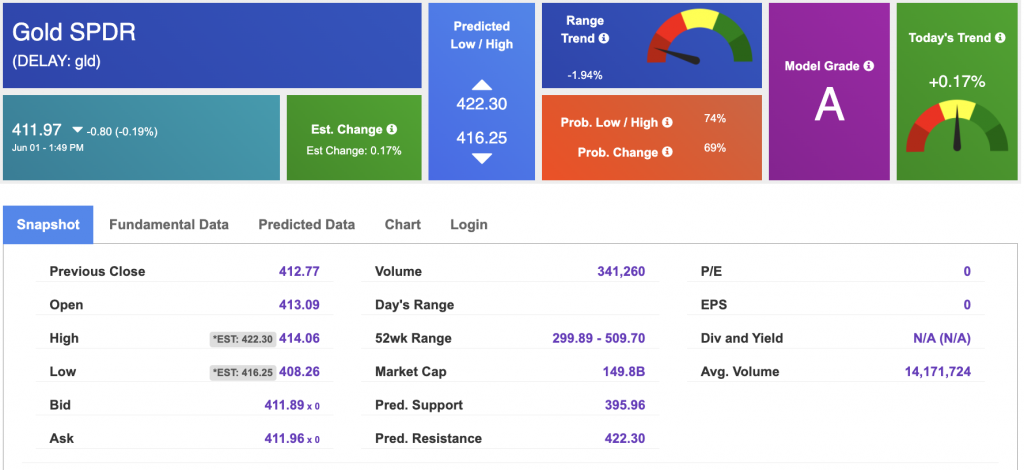

The price for the Gold Continuous Contract (GC00) is down 1.64% at $4,517.60 at the time of publication.

Using SPDR GOLD TRUST (GLD) as a tracker in our Stock Forecast Tool, the 10-day prediction window shows mixed signals. The gold proxy is trading at $411.97 at the time of publication. Vector signals show +0.17% for today. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

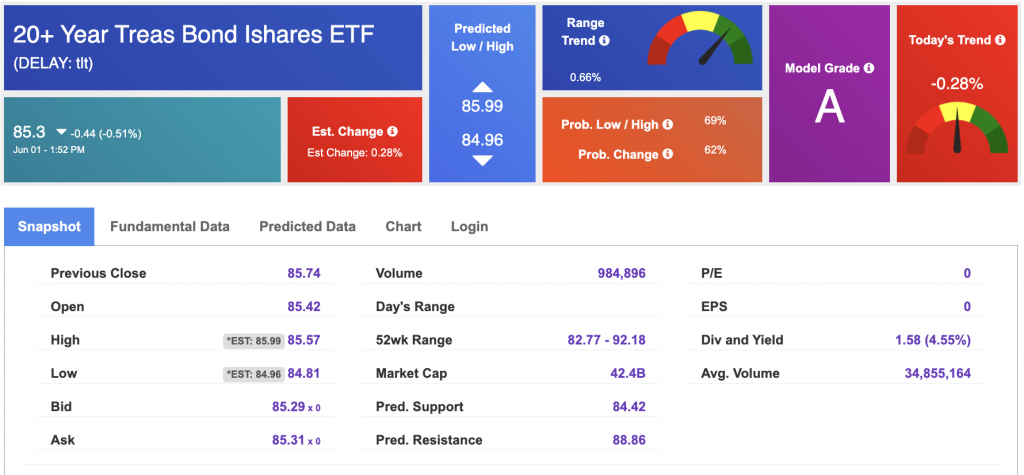

The yield on the 10-year Treasury note is up at 4.4477% at the time of publication.

The yield on the 30-year Treasury note is up at 4.993% at the time of publication.

Using the iShares 20+ Year Treasury Bond ETF (TLT) as a proxy for bond prices in our Stock Forecast Tool, we see mixed signals in our 10-day prediction window. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

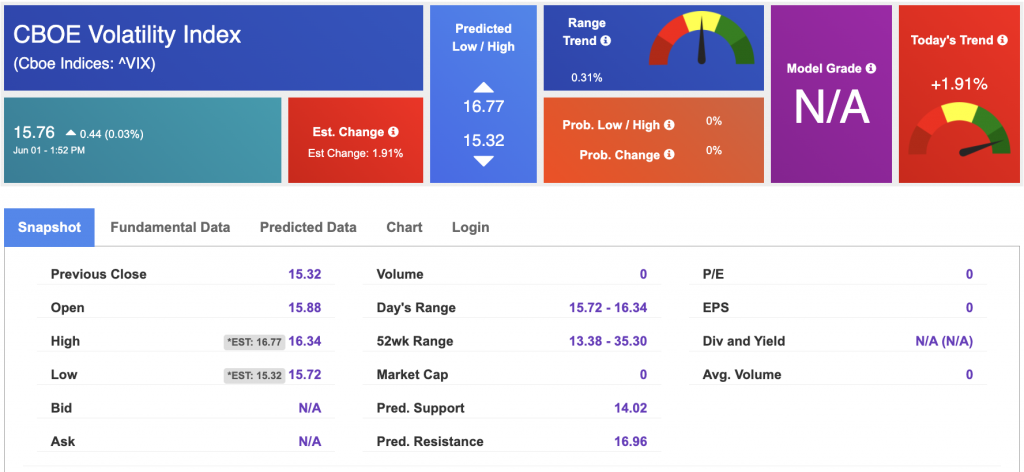

The CBOE Volatility Index (^VIX) is priced at $15.76 at the time of publication, and our 10-day prediction window shows mixed signals. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!