Sign Up for One-on-One Coaching and get our Premium Membership FREE for 1 Year!

CLICK HERE TO APPLY

Sign Up for One-on-One Coaching and get our Premium Membership FREE for 1 Year!

CLICK HERE TO APPLY

U.S. stocks opened the week with a rebound, led by technology and semiconductor names, as investors stepped back into the same AI-linked sectors that were hit hard at the end of last week. The move higher was encouraging, but it does not erase the bigger message from Friday: this market is still bullish, but it is becoming more sensitive to interest rates, inflation, oil prices, and stretched expectations in the AI trade.

SPY continues to trade near the upper end of our target range, with the rally still capable of reaching the $740–$760 area over the next few months if earnings remain strong, inflation cools, and buyers continue to defend leadership sectors. Short-term support remains in the $680–$700 range. As long as that area holds, the longer-term trend remains intact. I remain in the bullish camp, but this is not a market where investors should confuse momentum with safety. The right approach remains selective, disciplined, and risk-aware.

The biggest market-moving story from last week was the stronger-than-expected May jobs report. Nonfarm payrolls surged to 172,000, well above expectations near 85,000, while unemployment held at 4.3%. At first glance, that looks like good news for the economy. But for the market, it created a “good news is bad news” reaction because a stronger labor market makes it harder for the Federal Reserve to justify cutting rates. It also raises the risk that inflation remains sticky and that policy stays higher for longer.

That is why the 10-year Treasury yield remains one of the most important numbers on the screen. The 10-year has been volatile, trading in a wide range between roughly 3.6% and 4.50%, and last week’s jobs data pushed it sharply higher toward the mid-4% area. Higher yields create more pressure on growth stocks, especially the high-valuation technology and AI names that have led the rally. When yields rise quickly, investors begin to question how much they are willing to pay for future earnings.

The tech and AI trade also showed signs of fatigue last week. Chip stocks extended losses after Broadcom’s disappointing guidance failed to meet the market’s elevated expectations. Broadcom, Micron, Nvidia, and other semiconductor names sold off sharply, weighing heavily on the Nasdaq. This does not mean the AI rally is over. It does mean expectations are extremely high. Investors are no longer rewarding every AI-related story equally. The market is beginning to separate companies with real earnings power, strong demand, and clear AI monetization from names that have simply been carried higher by momentum.

Monday’s rebound in chip stocks was important because it showed that buyers have not abandoned the AI theme. Marvell Technology jumped after news that it will join the S&P 500 later this month, while several semiconductor and memory names recovered from Friday’s sharp pressure. That is a constructive sign. But the takeaway is still the same: the AI trade remains intact, but it is no longer moving in a straight line. After such a strong run, volatility should be expected.

Oil and geopolitics remain another key risk. U.S.-Iran headlines continue to send mixed signals, with optimism at times offset by reports of stalled progress and continued regional tension. The market received some relief Monday as oil pulled back from overnight highs after Iran signaled an end to offensive military operations against Israel. Still, crude remains elevated enough to keep inflation concerns alive. Oil matters because it filters through transportation costs, consumer prices, corporate margins, and inflation expectations. If oil rises again while Treasury yields remain high, the market could face another round of pressure.

Earnings and sector rotation also remain important. The tail end of earnings season has continued to show strength, especially in technology, but mixed results have created sharper reactions. Broadcom and CrowdStrike weakness helped trigger pressure in growth names last week, while strength in financials, healthcare, and defensive areas helped support the Dow. UnitedHealth, Goldman Sachs, and other value-oriented or defensive names showed relative strength as investors rotated away from the most crowded AI winners.

That rotation is healthy if it broadens the rally. A market led by only a handful of mega-cap technology names becomes fragile. A market where financials, healthcare, industrials, and defensives can also participate is more durable. The question now is whether rotation represents healthy broadening or whether it is an early sign that investors are reducing risk. This week’s inflation data may help answer that question.

The main events this week are CPI and PPI. CPI will give investors the next major read on consumer inflation, while PPI will provide a view into producer-level price pressure. These reports matter because the market is already priced for strength. If inflation comes in cooler than expected, yields could stabilize and the rebound in technology could continue. If inflation comes in hot, the market may quickly reprice around a more hawkish Fed, higher yields, and renewed pressure on growth stocks.

SpaceX IPO buzz is another major story to watch. Anticipation has built around what could be a massive offering, with reports pointing to a possible mid-June trading debut and a valuation that would immediately make it one of the most closely watched market events of the year. At the same time, S&P Dow Jones denied fast-track index inclusion, which limits the immediate passive-buying catalyst. This IPO could become a major test of investor appetite for high-growth, high-valuation stories at a time when the broader AI and tech trade is already showing signs of stress.

Apple is also in focus as its WWDC event centers on Apple Intelligence and Siri. Investors are looking for proof that Apple can strengthen its AI narrative and close the gap with other mega-cap technology leaders. The stock’s muted reaction shows that the market wants substance, not just headlines. In this environment, AI announcements need to translate into product adoption, revenue opportunity, and margin support.

The bottom line is that Monday’s rebound was constructive, but the market is not out of the woods. Labor market strength has reignited rate concerns. Oil and geopolitical headlines remain unstable. Inflation data is directly ahead. AI stocks are still leaders, but expectations are extremely high. And unemployment indicators are beginning to tick up around the edges, which keeps the soft-landing narrative from becoming too comfortable.

For investors, the playbook remains the same. Stay bullish, but do not be reckless. Respect the trend, but also respect the risks. Use pullbacks to identify leadership, not to chase weakness. Keep position sizes reasonable. Watch SPY’s $680–$700 support zone closely. If the market can hold that area and push through the $740–$760 zone with improving breadth, the longer-term rally remains intact.

This is a market that can still move higher, but it is also a market that will punish complacency. The rally remains alive, but inflation week will determine whether Monday’s rebound has real staying power or whether last week’s selloff was the first warning that valuations, yields, and geopolitical risk are starting to matter again.

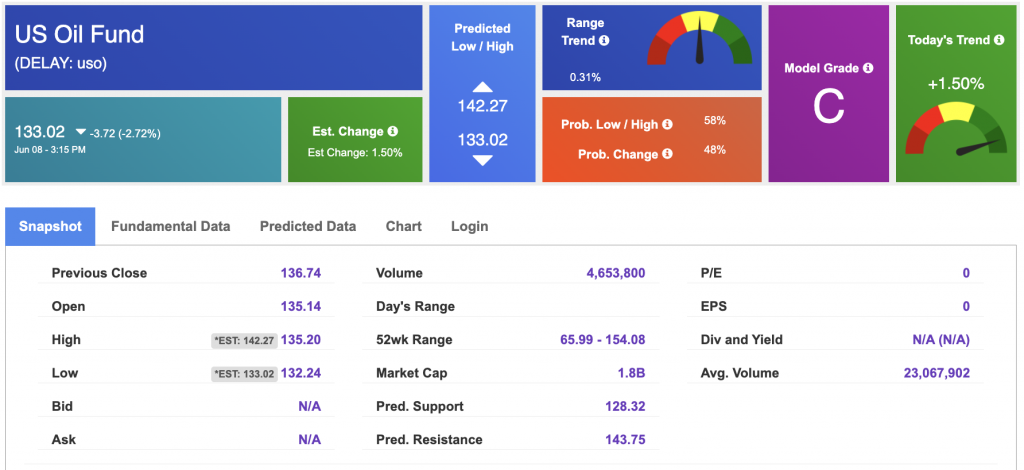

West Texas Intermediate for Crude Oil delivery (CL.1) is priced at $91.40 per barrel, up 0.98%, at the time of publication.

Looking at USO, a crude oil tracker, our 10-day prediction model shows mixed signals. The fund is trading at $133.02 at the time of publication. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

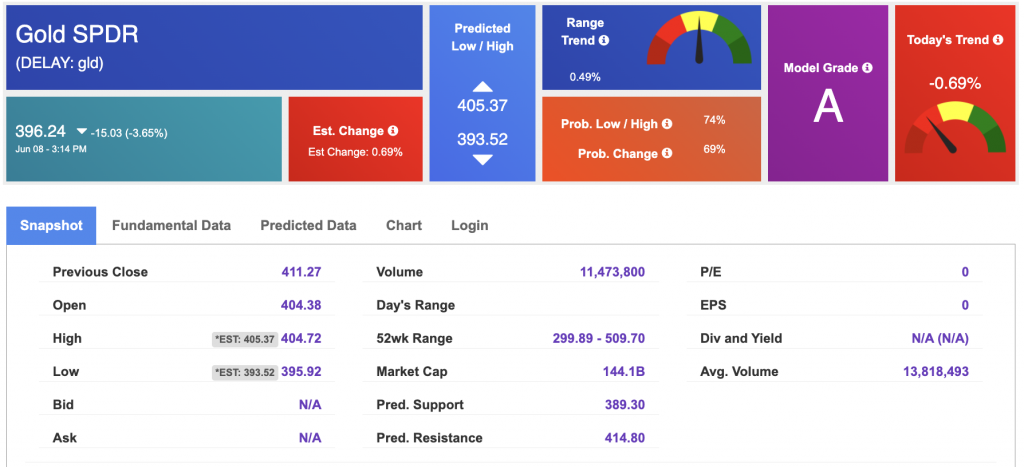

The price for the Gold Continuous Contract (GC00) is down 0.34% at $4,348.50 at the time of publication.

Using SPDR GOLD TRUST (GLD) as a tracker in our Stock Forecast Tool, the 10-day prediction window shows mixed signals. The gold proxy is trading at $396.24 at the time of publication. Vector signals show -0.69% for today. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

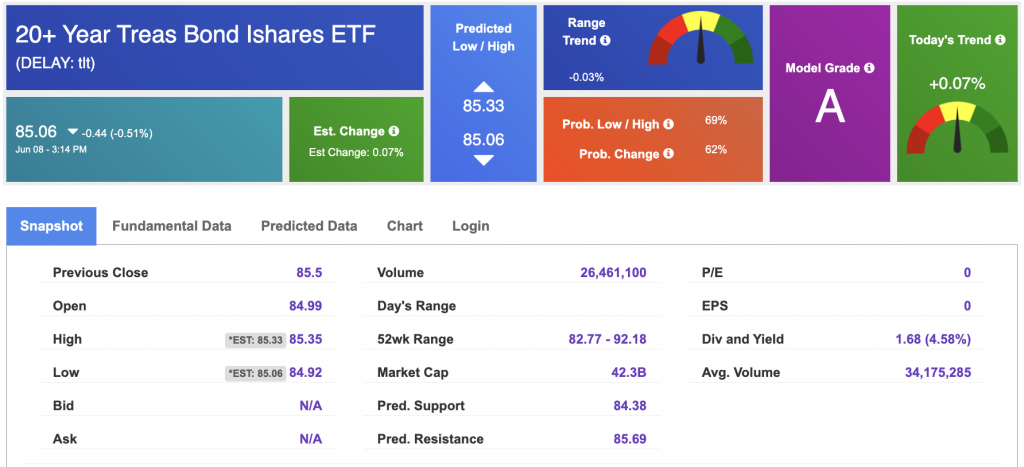

The yield on the 10-year Treasury note is up at 4.571% at the time of publication.

The yield on the 30-year Treasury note is up at 5.043% at the time of publication.

Using the iShares 20+ Year Treasury Bond ETF (TLT) as a proxy for bond prices in our Stock Forecast Tool, we see mixed signals in our 10-day prediction window. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

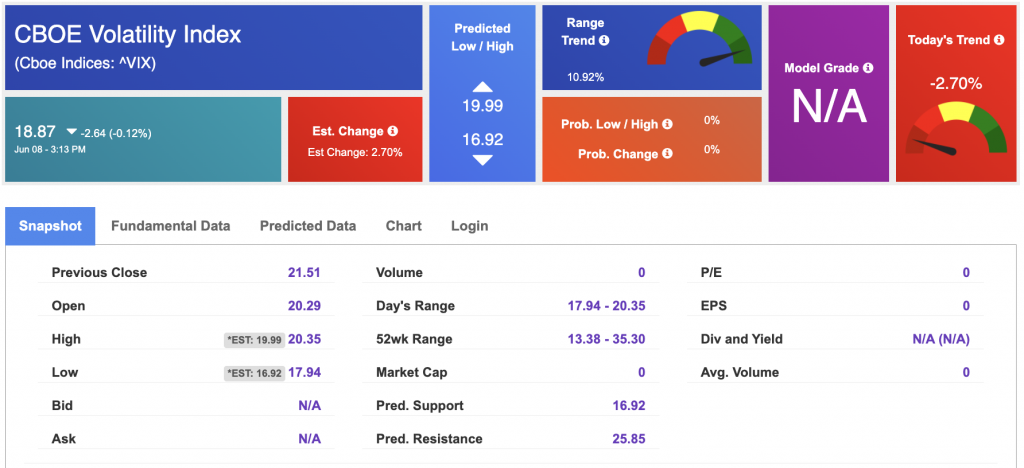

The CBOE Volatility Index (^VIX) is priced at $18.87 at the time of publication, and our 10-day prediction window shows mixed signals. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!