Save Big on Commissions ($0.65 per Contract)

CLICK HERE TO LEARN MORE

Save Big on Commissions ($0.65 per Contract)

CLICK HERE TO LEARN MORE

U.S. stocks are starting the week under pressure as oil prices surge, Iran tensions intensify, bond yields rise, and investors prepare for a critical round of Fed minutes, global PMI data, and mega-cap earnings. After last week’s push to fresh record highs, the market is now facing a more difficult test: whether strong earnings and AI leadership can continue to support equities while inflation risks, geopolitical shocks, and higher-for-longer interest rates return to the center of the conversation.

Last week, the market was still climbing through uncertainty. The major indexes pushed to fresh highs, AI momentum remained strong, and investors continued to buy dips despite ongoing concerns around Iran, tariffs, oil, and interest rates. The VIX near 17 suggested investors were alert but not panicking, and the broader trend remained bullish as earnings strength and technology leadership continued to support risk appetite.

But Monday’s setup looks different.

Markets are starting the week with a more defensive tone as the Iran conflict, oil prices, and global bond yields all move back into focus. Brent crude has climbed above $110 per barrel as supply fears tied to the Strait of Hormuz and broader Middle East tensions continue to pressure global energy markets. That matters because oil is no longer just a commodity story. It is now one of the most important macro variables shaping inflation expectations, Fed policy, consumer confidence, and equity valuations.

The main issue for investors is the same one we discussed last week: the market can handle uncertainty, but it becomes much harder when uncertainty feeds directly into inflation.

Higher oil prices increase the risk that inflation remains sticky or reaccelerates. That puts the Federal Reserve in a difficult position. If growth slows while inflation pressures rise, the Fed has less flexibility to cut rates and may even have to keep a tighter policy stance for longer. That is why bond yields are moving higher globally and why investors are paying close attention to this week’s FOMC minutes. Markets want to know whether Fed officials are beginning to think more seriously about renewed inflation pressure, oil-price shocks, and the possibility that rates may need to stay elevated longer than investors had hoped.

That is also why Friday’s selloff matters. The Dow, Nasdaq, and S&P 500 all closed lower as rising oil prices and renewed Iran concerns weighed on sentiment. Technology led the decline, with NVIDIA falling sharply as investors took profits ahead of this week’s major earnings report. That does not mean the AI trade is broken. But it does show that leadership stocks are no longer immune to macro pressure. When yields rise and inflation fears return, even the strongest growth names can come under pressure.

NVIDIA will be one of the most important earnings reports of the week. The company remains a central barometer for AI spending, semiconductor demand, data-center infrastructure, and overall technology leadership. If NVIDIA delivers strong results and guidance, it could help restore confidence in the AI-led rally. If the report disappoints or guidance comes in below elevated expectations, the market could see additional pressure in semiconductors and broader growth stocks.

Retail earnings will also matter. Walmart, Target, Lowe’s, TJX, Ross Stores, and Deere are all on deck this week, giving investors a broader read on consumer strength, household spending, margins, and how companies are handling higher input costs. In a market worried about oil, inflation, and mortgage rates, the consumer becomes even more important. Investors will want to know whether households are still spending, whether retailers are protecting margins, and whether higher energy costs are beginning to pressure demand.

Housing remains another area to watch. Mortgage rates have moved higher again, with the 30-year rate near 6.5%, and affordability remains a major challenge. Higher inflation and rising yields continue to keep pressure on the housing market, and Monday’s NAHB Housing Market Index will provide another read on builder sentiment. Housing has been one of the more sensitive parts of the economy because it sits directly at the intersection of rates, inflation, consumer confidence, and affordability.

The global backdrop is not helping either. China’s latest macro data showed weak retail sales, slowing industrial production, and falling fixed-asset investment, reinforcing concerns that global demand remains uneven. Eurozone flash PMIs later this week will help show whether activity in Europe is stabilizing or weakening further, while inflation data from the U.K., Canada, and Japan will influence central-bank expectations outside the U.S. This is no longer just a U.S. market story. Global inflation, energy prices, bond yields, and growth expectations are all connected right now.

For investors, the key question is whether this is a normal pullback within a strong uptrend or the beginning of a deeper shift in sentiment.

So far, the broader market trend remains constructive. Earnings have been strong, AI leadership remains intact, and investors have repeatedly shown a willingness to buy dips when the macro backdrop does not materially deteriorate. But the market is also more vulnerable now than it was a few weeks ago because expectations are higher, valuations are more stretched, and geopolitical risk has become more directly tied to inflation.

For SPY, I continue to believe the longer-term rally can work toward the $740–$760 area over the next few months if earnings remain strong, AI leadership continues, and oil does not create a more serious inflation shock. But short-term support in the $680–$700 zone is now especially important. A pullback into that area would not necessarily break the bullish trend, but it would test investor conviction and help reveal whether buyers are still willing to step in.

The biggest risk is not simply the Iran conflict, oil prices, tariffs, or interest rates by themselves. The bigger risk is the combination of all those pressures arriving at the same time. Higher oil can keep inflation elevated. Higher inflation can keep the Fed tighter for longer. Higher rates can pressure valuations. And if the labor market or consumer begins to weaken at the same time, the market could face a more complicated stagflation-style setup.

The FOMC minutes on Wednesday will be the top macro catalyst. Investors will look for any signs that Fed officials are becoming more concerned about renewed inflation pressure, energy shocks, or the possibility that policy may need to remain restrictive for longer. Flash PMIs on Thursday will help show whether business activity is holding up or slowing under the weight of higher costs and geopolitical uncertainty. Earnings from NVIDIA and major retailers will then determine whether corporate fundamentals remain strong enough to offset the macro risks.

Last week, record highs showed that investors still believed in the rally. This week, rising oil, Iran tensions, higher yields, and Fed uncertainty are testing that belief. The bull case is still alive, but it is no longer enough to simply point to AI strength and earnings momentum. Investors now need to see whether those positives can withstand a more difficult macro environment.

This remains a market with opportunity, but it is also a market that requires patience, risk management, and a clear process. Strong earnings and AI leadership can still support higher prices, but oil and interest rates are now the two variables that can quickly change the tone. If they stabilize, buyers may return quickly. If they continue to rise, the market may need more time to reset.

For now, I remain constructive on the long-term trend, but more cautious in the short term. The rally has not been broken, but it is being tested. And in this environment, the best approach is to stay focused on quality, respect support levels, watch the Fed closely, and avoid letting every headline force an emotional decision.

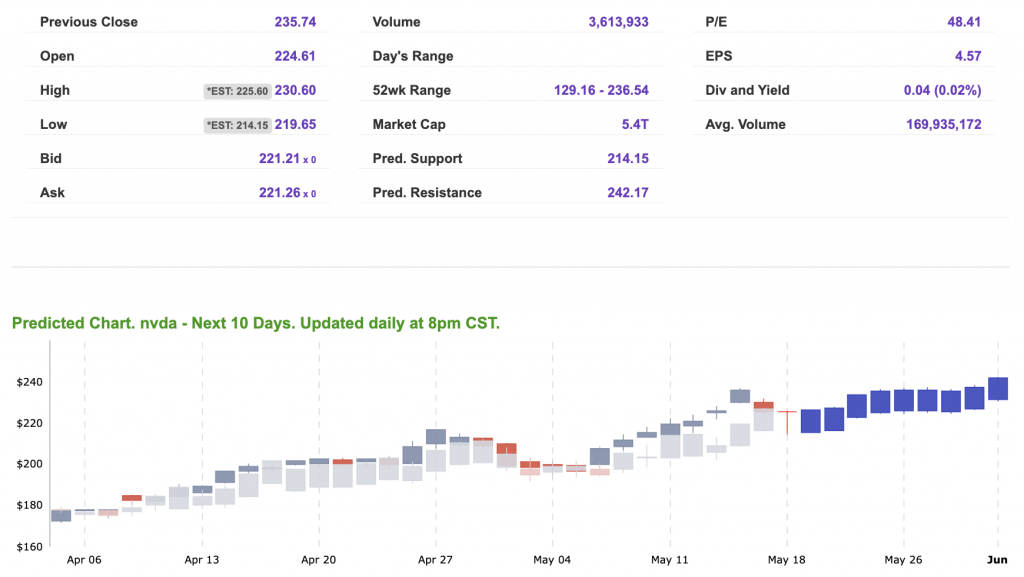

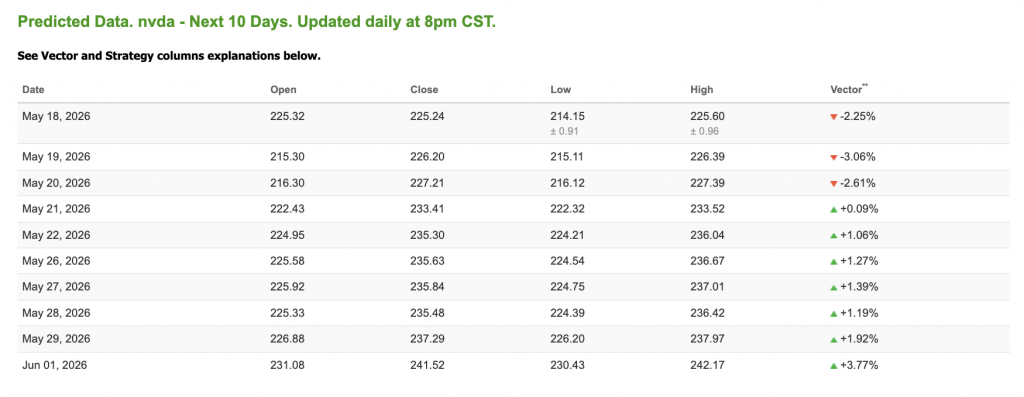

Our featured symbol for Tuesday is NVDA. NVIDIA Corp. (NVDA) is showing a steady vector in our Stock Forecast Toolbox’s 10-day forecast.

The symbol is trading at $221.25 with a vector of -2.25% at the time of publication.

10-Day Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Note: The Vector column calculates the change of the Forecasted Average Price for the next trading session relative to the average of actual prices for the last trading session. The column shows the expected average price movement “Up or Down”, in percent. Trend traders should trade along the predicted direction of the Vector. The higher the value of the Vector the higher its momentum.

*Please note: At the time of publication, Vlad Karpel does have a position in the featured symbol, NVDA. Our featured symbol is part of your free subscription service. It is not included in any paid Tradespoon subscription service. Vlad Karpel only trades his money in paid subscription services. If you are a paid subscriber, please review your Premium Member Picks, ActiveTrader, or MonthlyTrader recommendations. If you are interested in receiving Vlad’s picks, please click here.

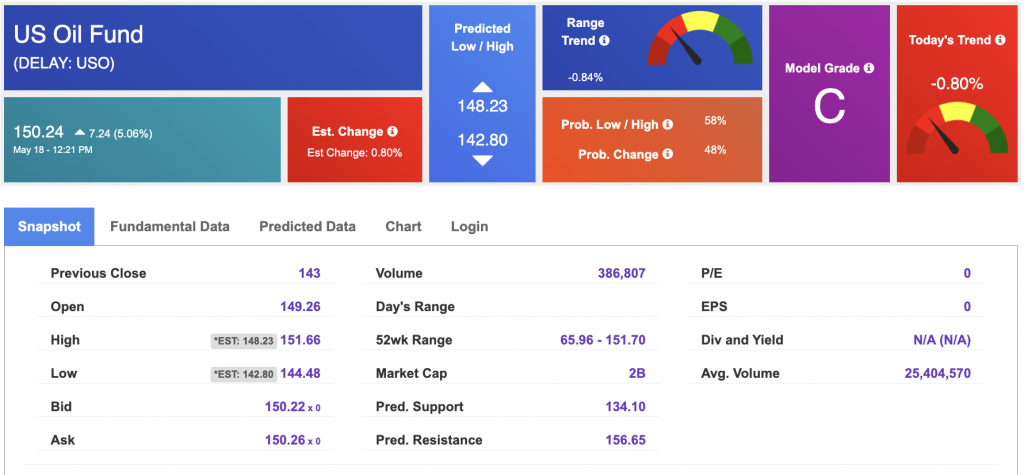

West Texas Intermediate for Crude Oil delivery (CL.1) is priced at $106.52 per barrel, up 8.15%, at the time of publication.

Looking at USO, a crude oil tracker, our 10-day prediction model shows mixed signals. The fund is trading at $150.24 at the time of publication. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

The price for the Gold Continuous Contract (GC00) is down 0.11% at $4.556.70 at the time of publication.

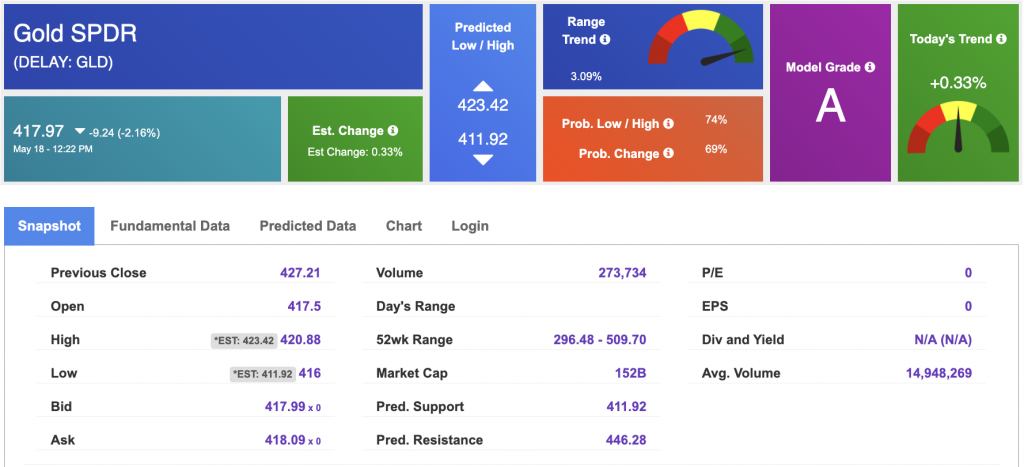

Using SPDR GOLD TRUST (GLD) as a tracker in our Stock Forecast Tool, the 10-day prediction window shows mixed signals. The gold proxy is trading at $417.97 at the time of publication. Vector signals show +0.33% for today. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

The yield on the 10-year Treasury note is up at 4.605% at the time of publication.

The yield on the 30-year Treasury note is up at 5.136% at the time of publication.

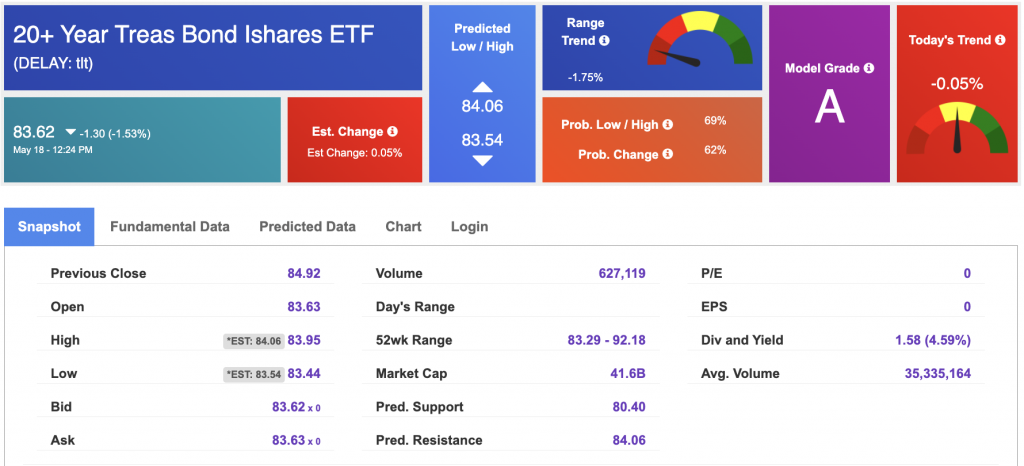

Using the iShares 20+ Year Treasury Bond ETF (TLT) as a proxy for bond prices in our Stock Forecast Tool, we see mixed signals in our 10-day prediction window. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

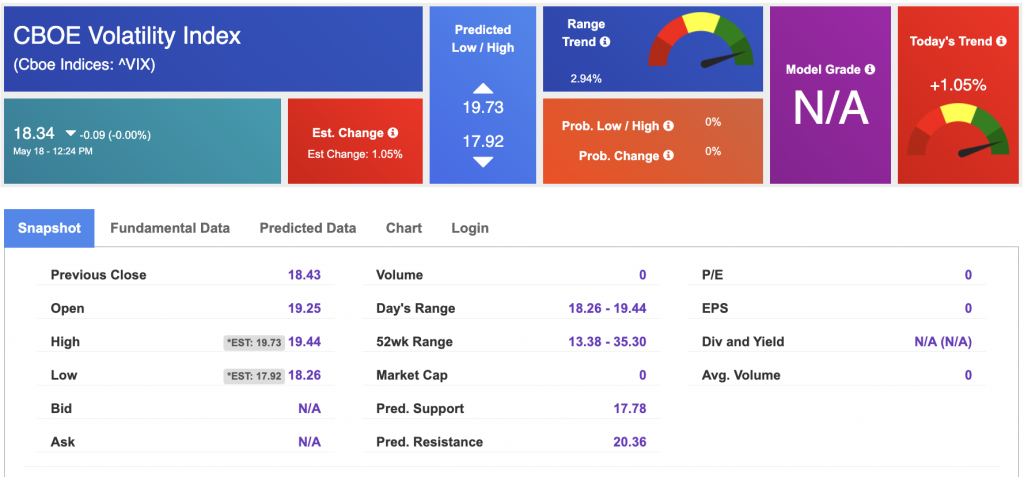

The CBOE Volatility Index (^VIX) is priced at $18.34 at the time of publication, and our 10-day prediction window shows mixed signals. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!