Are you a Long-Term Trader? Then take a look at our NEW RoboInvestor Service?

CLICK HERE TO LEARN MORE

Are you a Long-Term Trader? Then take a look at our NEW RoboInvestor Service?

CLICK HERE TO LEARN MORE

After the holiday-shortened week, momentum found semiconductors rallying, oil cooled, and weak jobs data reset rate expectations — but key macro reports could decide whether the rally has room to run.

Markets opened the holiday-shortened week on a strong note, with U.S. equities pushing higher after the Fourth of July break. The Nasdaq and S&P 500 led the move, the Dow traded near fresh record territory, and technology once again became the engine behind the rally. Semiconductors were the standout group, with AI-chip demand, memory strength, and renewed interest in the broader AI infrastructure trade helping lift the sector after last week’s profit-taking.

That rebound matters because technology remains the most important battleground for this market. Last week, semiconductors and memory-chip stocks came under pressure as investors rotated away from some of the biggest winners of the year. Today’s move shows that the AI trade is not broken, but it is becoming more selective. Investors are still willing to buy growth, but they are becoming more disciplined about which names deserve premium valuations and which names may have already moved too far too fast.

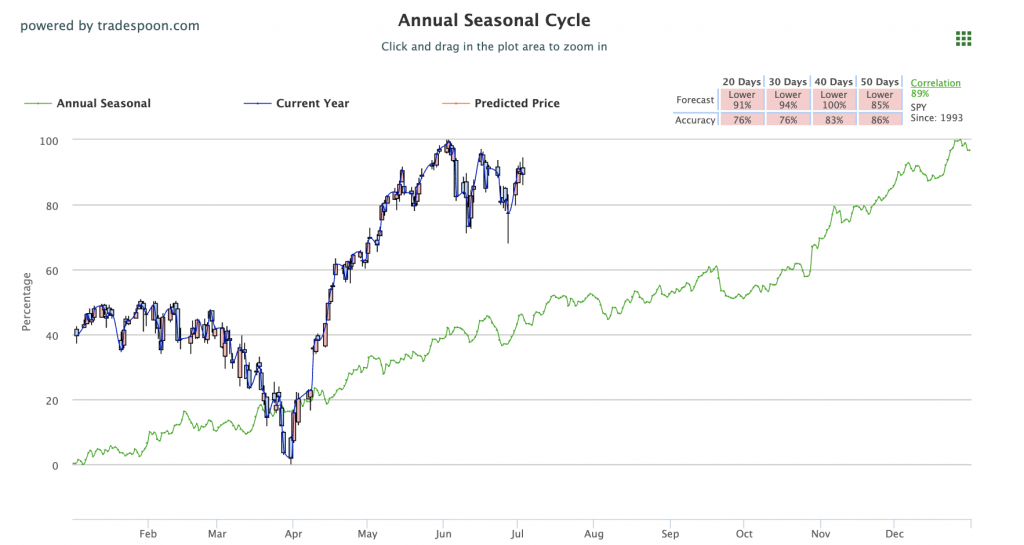

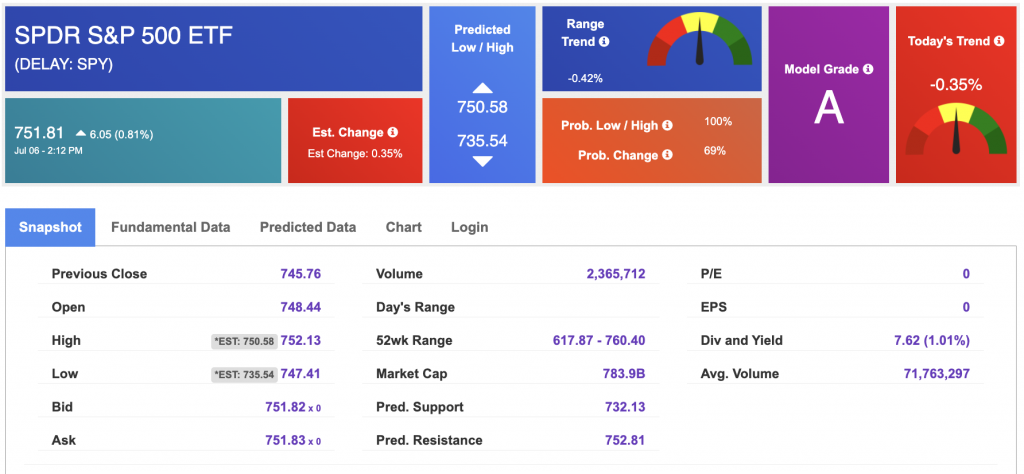

Markets are still trading near all-time highs, with the VIX recently around 18 and SPY holding a constructive long-term trend. I remain in the market-bullish camp, with SPY still capable of working toward the $760–$780 area over the next few months if earnings stay resilient, inflation continues to cool, and yields stabilize. At the same time, short-term support remains closer to the $700–$720 range, and investors should not ignore the risks building beneath the surface.

The biggest macro story remains the labor market. June payrolls came in far weaker than expected, with the economy adding only about 57,000 jobs versus expectations closer to 110,000. That kind of miss changes the market conversation. On one hand, softer jobs data reduces fears of additional Fed rate hikes and gives growth stocks more room to breathe. On the other hand, weak payrolls, lower participation, and signs of cooling hiring raise a different question: is the economy slowing faster than investors expected?

That is the tension driving this market. Bad news can still be good news for rates, but it is not automatically good news for the economy. The market wants enough weakness to keep the Fed patient, but not enough weakness to damage earnings, consumer spending, credit conditions, or business confidence. That is a narrow path, and it means every major economic report now carries more weight.

This week, the focus shifts to ISM Services PMI, the Federal Reserve meeting minutes, Chinese inflation data, global PMI readings, and follow-through from the weak labor report. With earnings season still light, macro data will likely dominate trading direction. The ISM Services report is especially important because the services side of the economy has been one of the key supports for growth. If services remain firm, it would help support the soft-landing case. If services weaken sharply, recession concerns could rise quickly.

Wednesday’s Fed minutes could also be a major market mover. Investors will be looking closely at the tone around inflation, labor conditions, financial conditions, and the future rate path. Fed Chair Warsh has reiterated the Fed’s commitment to the 2% inflation target, which means the market should not assume that weaker jobs data automatically creates an easier Fed. The Fed still needs inflation to move in the right direction, and the 10-year Treasury yield remains one of the most important variables for equities.

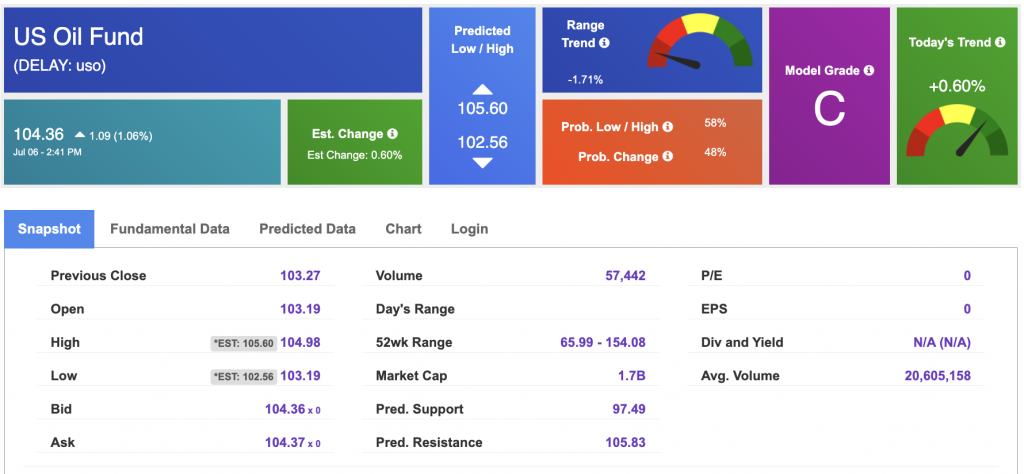

Oil is another key piece of the puzzle. Crude prices continued to slide, which helps ease inflation expectations and reduces pressure on consumers and businesses. Lower oil can support the bullish case by cooling headline inflation and reducing the risk of another energy-driven price shock. But energy weakness can also weigh on energy stocks, and geopolitical risk remains in the background. Any renewed escalation tied to Iran, tariffs, or global supply routes could quickly bring energy volatility back into focus.

Corporate signals remain mixed. Retail names like Macy’s and Kohl’s moved on restructuring and strategic updates, showing that investors are still trying to separate companies with credible turnaround plans from those facing deeper consumer pressure. Travel will also be in focus this week with Delta Air Lines earnings, which should offer a useful read on summer demand, consumer resilience, and discretionary spending. PepsiCo will provide another early look at whether consumers are still absorbing higher prices or beginning to trade down more aggressively.

That is why this remains a stock picker’s market. The major indexes can keep moving higher, but leadership is not universal. AI, semiconductors, infrastructure, and select technology names continue to attract capital, while retail, travel, energy, and more rate-sensitive areas remain more uneven. Investors should not assume that buying the broad market blindly will produce the same results as being selective with stronger setups.

The long-term trend is still constructive, and the market continues to give investors reasons for optimism. Semiconductors are rebounding, AI demand remains a powerful long-term theme, oil is easing, and weaker jobs data has reduced fears of another immediate Fed hike. But risks remain real. Labor data is cooling, yields are still volatile, earnings expectations are high, and the market is trading near record territory where disappointment can create sharp pullbacks.

My base case remains bullish, but disciplined. Investors do not need to abandon the market, but they do need a plan. This is an environment where emotional decision-making can become expensive, especially when headlines around the Fed, oil, jobs, and AI can shift sentiment quickly. A model-driven process can help separate signal from noise, identify stronger opportunities, and manage risk when volatility increases.

The market is starting the week with momentum, but this is not a simple risk-on environment. It is a selective rally, powered by AI and semiconductors, supported by lower oil, but still vulnerable to weak economic data and Fed uncertainty. Staying invested can still be the right approach, but discipline, selectivity, and risk management should remain at the center of every decision.

West Texas Intermediate for Crude Oil delivery (CL.1) is priced at $68.71 per barrel, up 0.04%, at the time of publication.

Looking at USO, a crude oil tracker, our 10-day prediction model shows mixed signals. The fund is trading at $104.36 at the time of publication. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

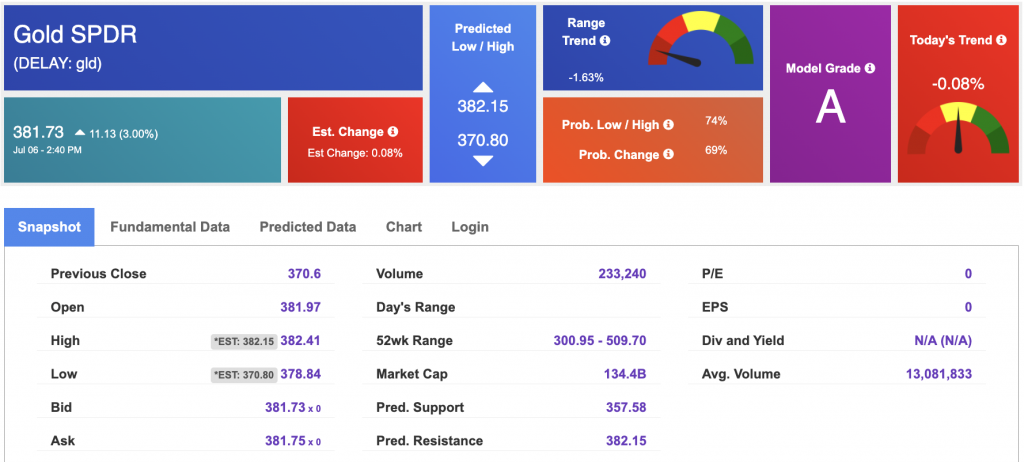

The price for the Gold Continuous Contract (GC00) is up 1.15% at $4,173.50 at the time of publication.

Using SPDR GOLD TRUST (GLD) as a tracker in our Stock Forecast Tool, the 10-day prediction window shows mixed signals. The gold proxy is trading at $381.73 at the time of publication. Vector signals show 0.00% for today. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

The yield on the 10-year Treasury note is down at 4.473% at the time of publication.

The yield on the 30-year Treasury note is up at 4.987% at the time of publication.

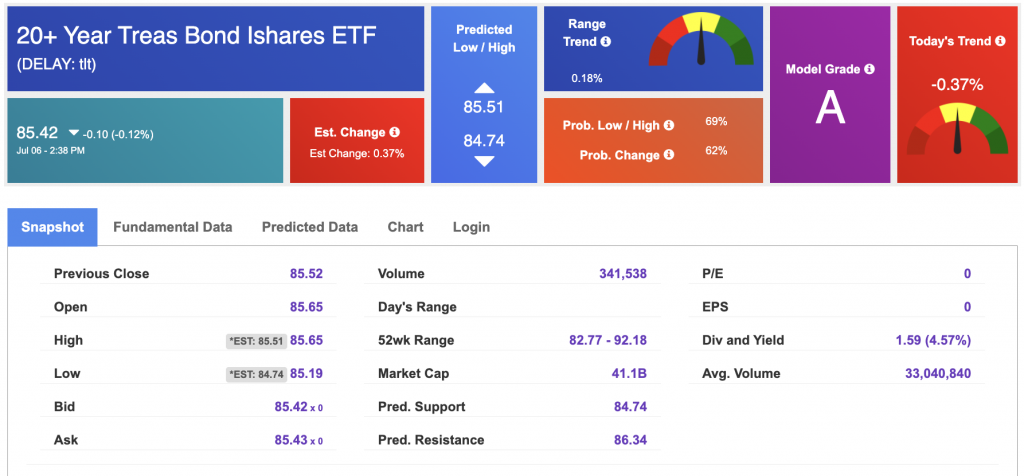

Using the iShares 20+ Year Treasury Bond ETF (TLT) as a proxy for bond prices in our Stock Forecast Tool, we see mixed signals in our 10-day prediction window. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

The CBOE Volatility Index (^VIX) is priced at $15.63 at the time of publication, and our 10-day prediction window shows mixed signals. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!