Save Big on Commissions ($0.65 per Contract)

CLICK HERE TO LEARN MORE

Save Big on Commissions ($0.65 per Contract)

CLICK HERE TO LEARN MORE

The market is starting the week with the same core tension that defined last week: investors still want to buy strength, but they are not ignoring the risks building underneath the surface.

On Monday, U.S. stocks continued to show resilience near record highs, with the S&P 500 and Nasdaq supported by another strong move in technology and semiconductor leadership. AI remains the central force behind market momentum. Nvidia, Intel, Qualcomm, Micron, and other chip-related names are helping keep the growth trade alive as investors continue to position around AI infrastructure spending, advanced memory demand, and the possibility of a broader semiconductor supercycle.

That leadership matters because this market has become increasingly selective. Investors are not buying every growth story blindly. They are rewarding companies tied to real demand, durable earnings power, and themes that can continue to attract institutional capital. Right now, AI chips and semiconductor infrastructure remain one of the clearest examples of that. Even with geopolitical risks elevated and oil prices rising, the market is still giving technology leadership the benefit of the doubt.

But the rally is not without pressure.

Oil remains one of the biggest risks facing the market this week. Crude prices moved higher again as tensions between the U.S. and Iran kept energy markets on edge. The Strait of Hormuz remains a key concern, and any prolonged disruption there can quickly feed into inflation expectations, transportation costs, corporate margins, and consumer sentiment. That is why oil is not just an energy story right now. It is a macro story, an inflation story, and a Federal Reserve story.

This is where Monday’s market setup becomes more complicated. On one side, AI strength is helping lift the Nasdaq and support the broader S&P 500. On the other side, higher oil prices are limiting how aggressive investors want to be ahead of this week’s inflation data. If oil stays elevated, the market may begin to worry that inflation progress could stall. If inflation stalls, the Fed has less room to ease policy. And if rates remain higher for longer, valuations near record highs become harder to justify.

That makes Tuesday’s CPI report the biggest catalyst of the week.

Investors are looking for confirmation that inflation remains under control despite the recent surge in energy prices. Expectations are for a hotter headline number, largely because of energy pressure, while core inflation is expected to remain more contained. That distinction will matter. If headline inflation jumps but core inflation stays steady, the market may look through part of the move as energy-driven. But if core inflation also comes in hotter than expected, that would be a bigger problem because it would suggest price pressure is spreading beyond oil.

A hotter CPI report could quickly shift the tone of the week. It could push Treasury yields higher, reduce confidence in near-term rate cuts, and pressure the same growth and technology names that have been leading the rally. A cooler or in-line report, however, would likely support the bullish case by giving investors more confidence that the Fed can eventually move toward easing without inflation reaccelerating.

That is why this week is so important. The market has already shown that it can absorb a lot: geopolitical tension, tariff uncertainty, higher energy prices, and a Federal Reserve that remains cautious. But with stocks near all-time highs, investors need fresh confirmation that the macro backdrop still supports risk assets. CPI, PPI, retail sales, jobless claims, industrial production, and consumer sentiment will all help shape that answer.

Earnings will also remain in focus. Major technology reports and updates from large-cap leaders will be watched closely because investors want to know whether AI spending is still translating into real revenue, strong margins, and confident guidance. The market has been willing to pay premium valuations for AI leadership, but that willingness depends on continued execution. Any signs of slowing demand or weaker guidance could create volatility, especially in names that have already moved sharply higher.

The Federal Reserve transition is another layer investors will need to monitor. Jerome Powell’s term as Fed Chair is nearing its end, and Kevin Warsh is expected to move toward confirmation as the next Fed Chair. That shift matters because markets are already debating how Fed policy could evolve under new leadership. Investors will be watching closely for any signal that the Fed may become more open to rate cuts, but the inflation data still has to cooperate. No Fed Chair can easily justify easier policy if energy-driven inflation becomes a broader problem.

For now, the broader trend remains constructive. The market is still acting well, AI leadership remains powerful, earnings have been strong enough to support risk appetite, and investors continue to buy dips when the fundamental story remains intact. That supports the bullish case.

But this is still a disciplined bullish market, not a careless one.

Oil near elevated levels, the Strait of Hormuz risk, U.S.–Iran uncertainty, tariff pressure, and this week’s CPI report all have the potential to change the tone quickly. If inflation data comes in hotter than expected or energy prices continue to rise, the market could see a near-term pullback even if the longer-term trend remains intact. If CPI comes in under control and earnings continue to support the AI narrative, the rally can continue to broaden and push higher.

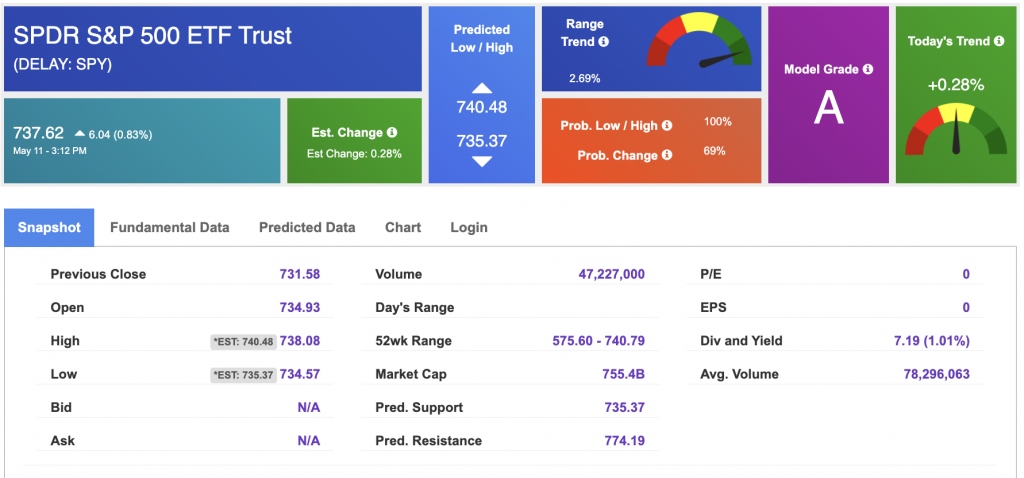

My outlook remains bullish, but selective. SPY still has room to move higher if earnings momentum continues, AI leadership remains intact, and macro risks stay contained. The $740–$760 area remains a possible upside target over the next few months. On the downside, the $660–$680 range remains the key support zone to watch if volatility returns.

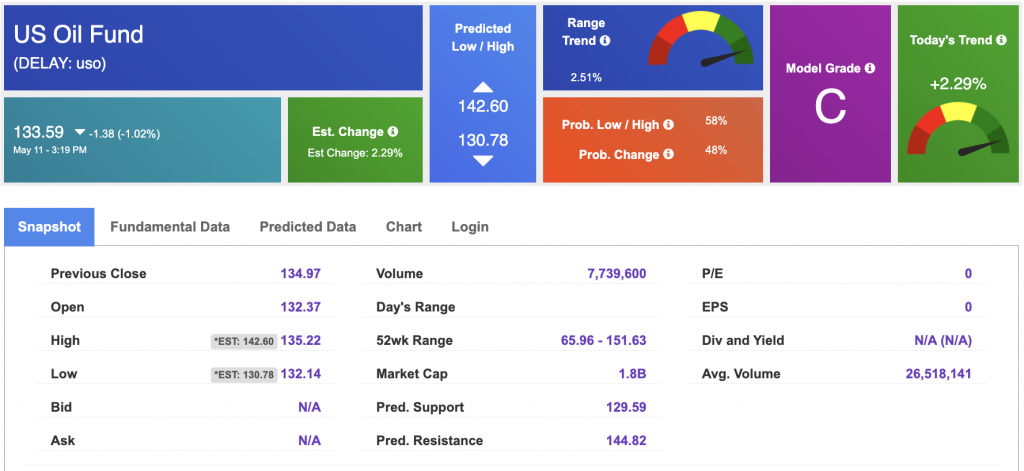

West Texas Intermediate for Crude Oil delivery (CL.1) is priced at $98.57 per barrel, up 3.30%, at the time of publication.

Looking at USO, a crude oil tracker, our 10-day prediction model shows mixed signals. The fund is trading at $133.59 at the time of publication. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

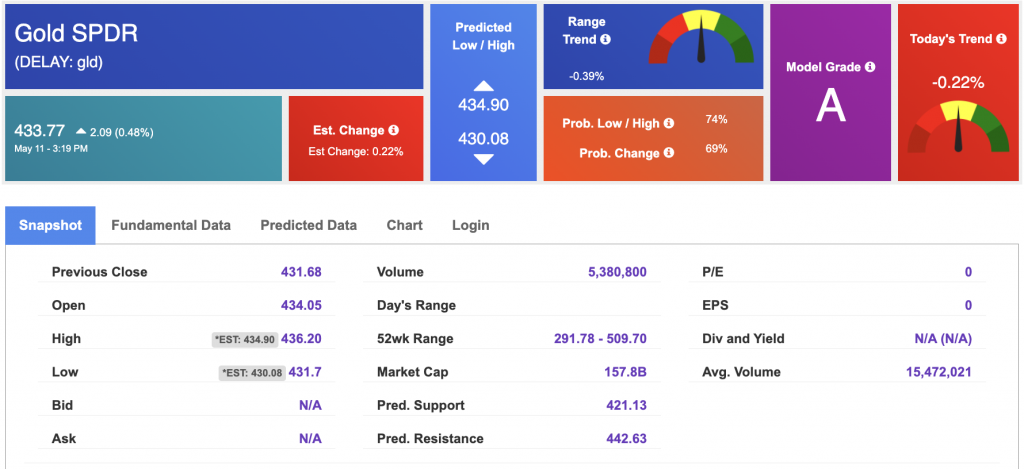

The price for the Gold Continuous Contract (GC00) is up 0.29% at $4,744.40 at the time of publication.

Using SPDR GOLD TRUST (GLD) as a tracker in our Stock Forecast Tool, the 10-day prediction window shows mixed signals. The gold proxy is trading at $433.77 at the time of publication. Vector signals show -0.22% for today. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

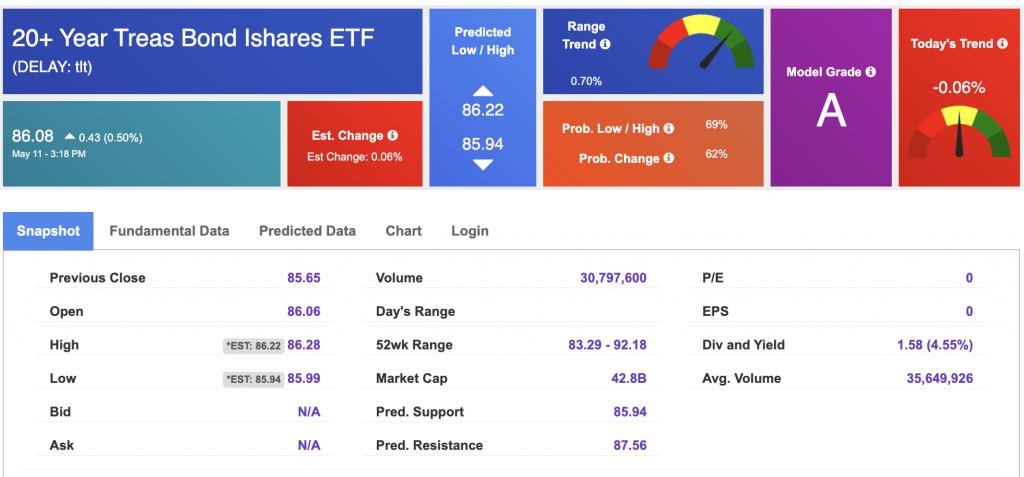

The yield on the 10-year Treasury note is up at 4.413% at the time of publication.

The yield on the 30-year Treasury note is up at 4.983% at the time of publication.

Using the iShares 20+ Year Treasury Bond ETF (TLT) as a proxy for bond prices in our Stock Forecast Tool, we see mixed signals in our 10-day prediction window. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

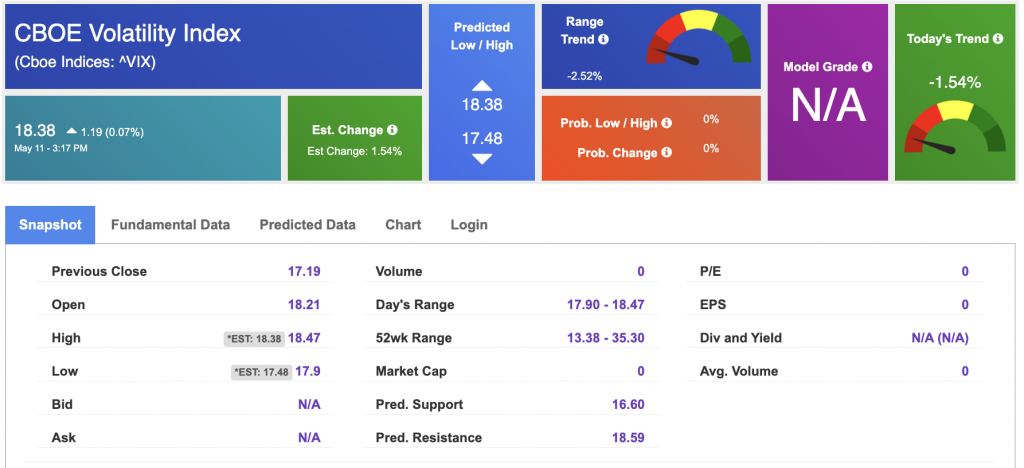

The CBOE Volatility Index (^VIX) is priced at $18.38 at the time of publication, and our 10-day prediction window shows mixed signals. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!