Special Offer: Try the 'RoboInvestor Membership' for ONLY $37!

CLICK HERE TO LEARN MORE

Special Offer: Try the 'RoboInvestor Membership' for ONLY $37!

CLICK HERE TO LEARN MORE

Oil shocks, tariff pressure, fading momentum, and a Fed that still cannot fully relax have turned this market into a far more selective battleground. Here is what really drove stocks this week, what the key economic data is saying, and why I remain market-neutral even with the long-term trend still intact.

Stocks tried to stabilize this week, but the bigger picture remained far less convincing than a few rebound days might suggest. Under the surface, the market continued to wrestle with the same difficult mix of forces: war in Iran, disruption around the Strait of Hormuz, elevated oil prices, tariff uncertainty, uneven earnings reactions, stubborn inflation risk, volatile Treasury yields, and a Federal Reserve that still does not have the freedom many investors were hoping for. The result has been a market that can bounce sharply on relief, yet still feels fragile underneath.

The week began with investors already in a cautious mood. By Monday, the dominant story was still the conflict involving Iran and the threat to one of the world’s most important energy corridors. Disruption in and around the Strait of Hormuz pushed oil sharply higher earlier in the period, at one point sending crude into territory that immediately revived inflation fears. Even though prices later pulled back from their most extreme levels as traders responded to signs that some transit might resume and emergency supply responses were being discussed, the damage to sentiment had already been done. Once the market sees energy prices spike like that, it starts recalculating everything from inflation expectations to Fed policy to consumer pressure.

And remember, we’re not talking about day trading here. I’m looking for 50-100% gains within the next 3 months, so my weekly updates are timely enough for you to act.

That is what made the early-week rebound less convincing than it looked on the surface. Stocks rose when oil eased, and technology names helped support the move, but it did not feel like a true macro reset. It felt like a relief rally. There is a major difference between a market recovering because the outlook has improved and a market simply reacting to one pressure point becoming temporarily less severe. This week leaned much more toward the second category.

As the days moved forward, that distinction became even clearer. The market was not just digesting geopolitical headlines. It was trying to process a much more complicated equation. Higher oil prices were showing up at a time when economic momentum was already less convincing, inflation risks were still lingering, and the Fed remained cautious. That is the kind of setup that brings stagflation concerns back into the conversation. If growth alone were slowing, investors could lean more comfortably into the idea of eventual rate cuts. If oil alone were rising, markets might simply rotate into energy and related defensive areas. But when slower growth, rising energy costs, and sticky inflation all show up together, it becomes much harder for equities to find a clean direction.

That tension shaped the entire week. Investors had to constantly weigh whether the latest market move was driven by improving fundamentals or simply by a temporary cooling in fear. Comments suggesting the Iran conflict might de-escalate helped fuel some of the week’s strongest relief rallies. Those moments mattered because they showed that investors still want to buy weakness when given a credible reason. But none of those rallies ever felt fully trusted, because the underlying uncertainty never actually disappeared. The risk to shipping, energy infrastructure, and broader regional escalation remained on the table throughout the week, which kept markets highly sensitive to every new headline.

At the same time, the macro backdrop did not provide enough reassurance to offset that uncertainty. This week’s economic reports reinforced the idea that the economy is still functioning, but with rising friction. Producer inflation came in hot enough to keep inflation concerns alive, especially with energy prices already adding another layer of pressure. Manufacturing data showed only modest progress rather than broad strength. Housing remained under pressure, with mortgage rates elevated and residential activity still lacking consistency.

The labor market has not collapsed, but it is no longer providing the same clean signal of strength it once did. Layoffs remain relatively contained, yet continuing claims have risen and unemployment indicators have started to drift higher. That is not recession confirmation, but it is enough to keep the market from feeling comfortable.

This is also where your view becomes especially important. You remain in the market-neutral camp because momentum has clearly deteriorated, and that deterioration now matters more than broad bullish narratives. The risk is not simply that the Fed keeps rates elevated. The bigger issue is that rates may stay higher for longer at the same time unemployment indicators begin to weaken and economic activity loses momentum. That is the kind of combination that can produce a much more selective and frustrating market even if the longer-term structure has not fully broken.

The Federal Reserve meeting only reinforced that tension. Rates were left unchanged, but the broader message was still cautious. Inflation expectations remain uncomfortable enough that policymakers cannot easily pivot into a clearly supportive stance. At the same time, the economy is showing just enough softening to keep investors questioning whether policy is too tight for the environment ahead.

That is why Treasury yields continue to matter so much. The 10-year has been volatile, swinging in a wide range between roughly 3.6% and 4.35%, and that instability has added another layer of uncertainty to equities. Markets can handle high yields more easily when growth is strong and broad. They struggle more when yields are volatile and growth is becoming less reliable.

Market sentiment this week reflected that exact struggle. This was not a panic tape, but it was not a comfortable one either. With the VIX around 25 and the major indexes trading near their 100-day moving averages, investors were clearly engaged but no longer fully in control. Buyers showed up, but conviction was inconsistent. Rallies lacked clean follow-through. Leadership narrowed. Risk appetite became much more selective. That is often what happens when the market is trying to decide whether it is dealing with a temporary geopolitical shock or a broader shift in the macro regime.

Under the surface, sector rotation told an important story. Energy was one of the strongest areas because of the oil spike, while many consumer-facing and growth-sensitive groups felt heavier. Materials came under pressure as the commodity shock created new uncertainty. Travel and airline stocks saw some rebound attempts after earlier weakness, but they remained vulnerable to energy volatility. Financials were also under pressure at times, as markets weighed the broader impact of slower growth, higher-for-longer policy, and policy noise around consumer finance.

Technology remained the most interesting area because it continued to show selective resilience rather than broad leadership. Nvidia remained in focus as enthusiasm around AI spending stayed alive, helped by the headlines generated at GTC and the ongoing market belief that the AI infrastructure buildout still has room to run. Micron was another major name this week, not just because of earnings, but because it highlighted how demanding this market has become. Even strong AI-driven results are no longer guaranteed to produce a clean positive reaction if investors become concerned about spending levels, margins, or capital intensity. That is one of the clearest signs that we are no longer in an easy momentum environment. Good stories still matter, but now they have to survive much tougher scrutiny.

Jabil added to that same theme from a different angle. Its results and outlook helped reinforce the idea that demand tied to AI data center infrastructure remains one of the market’s more durable support pillars. In a week filled with macro anxiety, that mattered. It showed that investors are still willing to reward companies exposed to real, ongoing secular demand. But again, the reaction was more selective than broad. That is the key difference. The AI trade is still alive, but investors are no longer rewarding the whole space equally. They are looking for execution, visibility, and earnings durability.

On the consumer side, Lululemon also carried weight this week because it offered a look into how tariffs, pricing, and demand may interact in a more difficult environment. Even when a company suggests it can absorb much of the direct tariff impact, investors still have to ask what those costs mean for margins, for pricing flexibility, and for consumer behavior. That is part of why tariffs matter even when they are not the lead story of the day. They add to the same inflation-sensitive atmosphere already being driven by oil and global instability. The market is not just pricing one challenge right now. It is trying to digest several overlapping pressures at once.

That is why overall market sentiment has remained more defensive than outright bearish. Investors are not acting as though the long-term bull market is completely broken, but they are also no longer treating every dip like an automatic opportunity. The easy upside environment has clearly cooled. This is now a market that demands more proof. Companies need to show durable earnings. Sectors need to show real relative strength. Macro data needs to hold up enough to prevent a deeper growth scare. And energy prices need to stop reintroducing inflation pressure every time investors start to calm down.

From my perspective, the long-term trend is still intact, but the near-term setup deserves respect. I still believe the SPY can eventually work toward the 700 to 720 area if inflation settles, yields calm down, and the geopolitical premium fades. That larger upside path is still possible. But for now, the far more important issue is whether support in the 620 to 650 zone can hold over the next few months. If that area remains intact, then this period can still be viewed as a difficult but manageable correction within a broader uptrend. If that support starts to break under the combined weight of sticky inflation, elevated energy costs, higher-for-longer rates, and weakening labor conditions, then the market likely stays trapped in a far more volatile, rotational, and selective regime.

That is why I remain market-neutral. Momentum has deteriorated enough to justify caution, even if the bigger structure has not yet fully failed. The main risk to the market remains that interest rates stay elevated while unemployment indicators continue to weaken. If that happens, investors are going to have a much harder time sustaining a broad rally. In that kind of environment, stock picking matters more, sector leadership narrows, and failed breakouts become more common.

The biggest takeaway from this week is that this is no longer a liquidity-driven tape where broad exposure does most of the work. It is a market demanding discipline, selectivity, and patience. There are still opportunities, especially in areas supported by real earnings strength and secular demand, but investors can no longer assume the entire market will rise together. This is a much more skill-based environment. Quality matters more. Durability matters more. Process matters more.

The market still wants to stabilize, and you can see that in every rebound attempt. But until oil, inflation, rates, and growth stop pulling against each other, caution deserves a seat at the table.

That’s exactly where RoboInvestor delivers an edge. Designed for a choppy, headline-sensitive environment, our AI-powered advisory zeroes in on statistically grounded setups with clearly defined risk-reward. It keeps you engaged without drifting into overtrading, helping you act with precision rather than react to noise.

Every other weekend, you’ll receive the RoboInvestor newsletter—a concise, high-signal read with market context, technical outlooks, updates on open positions, and clear, actionable trade ideas. Hence, you’re prepared and confident heading into Monday’s open.

Explore our latest forecasts, trade signals, and live strategy sessions at Tradespoon.com. Navigate uncertainty with confidence—and position yourself ahead of the curve.

Whether you’re targeting blue-chip stocks, ETFs, commodities, or inverse ETFs, RoboInvestor offers a flexible, forward-looking approach tailored to today’s market conditions. Our model portfolio typically holds 12 to 25 carefully selected positions, and we’ve recently adopted an even more selective strategy—focused on quality, resilience, and opportunity.

Join us and take advantage of advanced AI technology to guide your investments with precision and confidence.

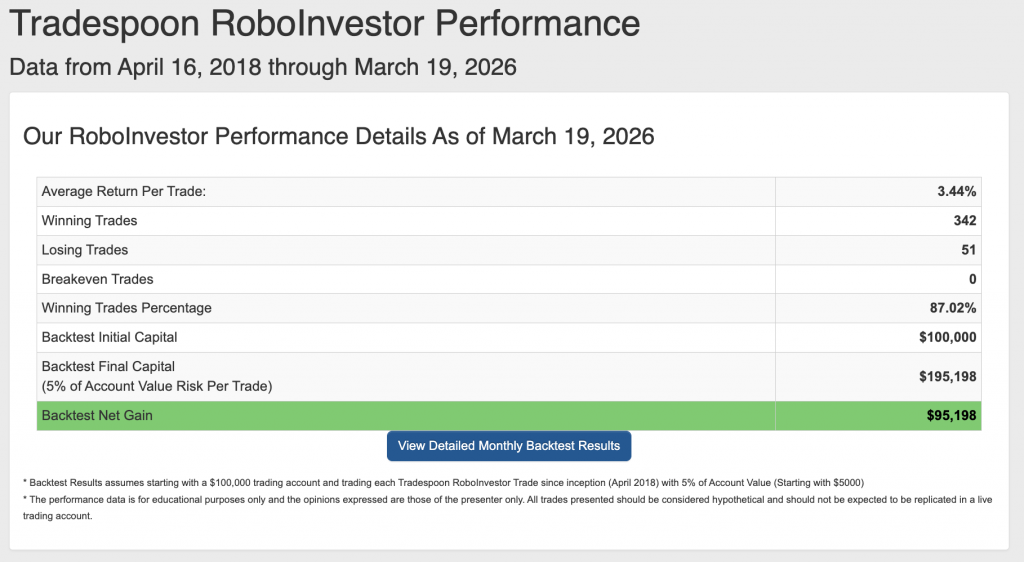

Our track record is one of the best in the retail advisory industry, with a Winning Trades Percentage of 87.02% since April 2018.

As we move toward Q2 2026 and geopolitical headlines continue to dominate the narrative, investors are navigating a market that appears stable on the surface yet increasingly selective beneath it. Tariff concerns briefly weighed on sentiment before easing, megacap earnings drew a sharper line between winners and laggards, and the Fed’s trajectory has grown less forgiving as inflation expectations stay stubborn. Interest rates have shifted from background noise to a defining variable, labor-market signals are softening at the edges, and market leadership is narrowing as investors demand a more direct link between spending, margins, and profits.

Volatility remains contained but reactive, quick to spike around policy shifts, earnings surprises, and moves in the bond market. In this environment, earnings quality and forward guidance are doing the real work of setting direction. Navigating the first quarter will require a disciplined, insight-driven approach that respects the influence of rates, manages employment risk, and stays flexible enough to participate in rotation without chasing fragile momentum.

Whether you are a seasoned investor or just starting, our team is here to help you every step of the way. Don’t face the challenges of tomorrow alone–join RoboInvestor today and take your investing to the next level.

Stay alert, stay strategic—and trade smart.

And remember, we’re not talking about day trading here. I’m looking for 50-100% gains within the next 3 months, so my weekly updates are timely enough for you to act.

*Please note: RoboStreet is part of your free subscription service. It is not included in any paid Tradespoon subscription service. Vlad Karpel only trades his own personal money for paid subscription services. If you are a paid subscriber, please review your Premium Member Picks, ActiveTrader, MonthlyTrader, or RoboInvestor recommendations. If you are interested in receiving Vlad’s personal picks, please click here.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!