Special Offer: Try the 'Picks Membership' for ONLY $37!

CLICK HERE TO LEARN MORE

Special Offer: Try the 'Picks Membership' for ONLY $37!

CLICK HERE TO LEARN MORE

RoboStreet – Weekly Market News & Sentiment: Geopolitical escalation, rising inflation risk, weakening labor data, and unstable rate expectations are colliding at once, pushing stocks into a more fragile, defensive, and headline-driven environment.

Markets entered the week on a fragile footing as geopolitical risk abruptly returned to the center of the macro narrative. After attempting to stabilize late last week, investors were hit on Monday with a fresh oil shock as crude surged above $110 per barrel on fears that the conflict involving Iran, Israel, and the United States could disrupt energy flows through the Strait of Hormuz.

That immediately revived inflation concerns just as markets had been hoping price pressures were beginning to cool. Equity futures sold off sharply at the start of the week, with the Dow under heavy pressure and both the S&P 500 and Nasdaq moving lower as investors repriced the balance between geopolitical risk and economic resilience.

And remember, we’re not talking about day trading here. I’m looking for 50-100% gains within the next 3 months, so my weekly updates are timely enough for you to act.

The oil move mattered well beyond the commodity complex. Higher crude prices create a direct threat to the disinflation story by lifting transportation, manufacturing, and consumer input costs at the exact moment investors are still trying to gauge whether the Federal Reserve can ease policy later this year.

In that sense, the rally in oil was not just an energy story. It quickly became a macro shock that affected equities, bonds, and currencies all at once, forcing markets to reassess inflation expectations, growth assumptions, and the path of interest rates. Treasury yields remained volatile within a broad range, and that volatility kept pressure on valuation-sensitive areas of the market, especially growth stocks.

By early in the week, sector behavior was already reflecting that shift. Energy shares drew renewed attention as investors recalibrated earnings potential for refiners, oil-service companies, and integrated producers. At the same time, many of the rate-sensitive leadership names that had powered the broader rally came under pressure as the market rotated toward cash-flow durability and defensive balance sheets. Utilities, staples, and healthcare also stood to benefit if volatility persisted, while the Nasdaq continued to feel the weight of higher-for-longer rate fears.

As the week progressed, the macro backdrop became even more fragile. Volatility climbed further, with the VIX pushing to around 25, a clear sign that markets were no longer trading in a calm repricing environment but in a more stressed, headline-driven tape. The major indices drifted closer to their 100-day moving averages, reinforcing the sense that the market’s momentum had deteriorated. The long-term structure has not broken, but the near-term trend has clearly become more unstable, with buyers losing some control as geopolitical headlines, oil swings, and rate expectations drive sharp intraday reversals.

The conflict in the Middle East remained the dominant catalyst throughout the week. Concerns over military escalation and disruption around the Strait of Hormuz, a key chokepoint for global oil flows, kept energy markets extremely volatile. Oil prices swung wildly as investors reacted to every new development, including reports tied to naval security, military positioning, and uncertainty over how long the conflict might drag on.

At various points, those fears pushed both Brent and WTI sharply higher, intensifying concerns that a prolonged energy shock could create a stagflationary backdrop in which growth slows while inflation stays sticky enough to prevent the Fed from easing aggressively.

There was one notable relief rally when comments from President Trump suggested the conflict could end sooner than initially feared. That briefly calmed markets, sent oil prices off their highs, and helped major indices recover from deep intraday losses. The rebound showed that investors remain eager to buy stabilization when they see it.

But that optimism did not fully hold. By midweek and into Thursday, conflicting headlines and the absence of a durable de-escalation path brought uncertainty right back into the market. Stocks turned choppy again, and by Thursday afternoon the Dow was down more than 550 points, while the S&P 500 and Nasdaq were also under heavy pressure as another jump in oil prices reignited fears that the economic damage from the conflict could extend well beyond the energy market.

At the same time, incoming economic data did little to fully calm nerves. Weak labor data earlier in the period raised fresh concerns that the economy may be losing momentum beneath the surface, while the latest inflation report showed price pressures still running above the Fed’s comfort zone.

Even if the CPI reading itself was not a major shock, it arrived in a context where energy inflation suddenly matters much more. That kept rate-cut hopes restrained and reinforced the idea that policy may stay tighter for longer than equity markets would prefer. In other words, the market is now facing pressure from both sides: rising inflation risks tied to oil and softer growth signals tied to employment and demand.

That combination is what makes this environment especially difficult. Wall Street is increasingly worried that if oil remains elevated for long enough, it could squeeze consumers, pressure margins, and worsen already fragile sentiment without giving the Fed room to respond. That is the core stagflation risk now hanging over the market. Rate-cut expectations have become more cautious, and that matters because the market’s strongest areas over the last year have depended heavily on falling inflation, steady growth, and the assumption that policy would gradually ease. Once any one of those pillars weakens, leadership narrows quickly.

Under the surface, that narrowing is already visible. The Magnificent Seven and other high-duration growth names have struggled to maintain leadership as yields and oil both move higher. Some technology and software areas have shown resilience at times, but the broader tone has shifted away from momentum chasing and toward a more selective, fundamentals-driven tape.

Energy remains a relative winner in this backdrop, while more cyclical and consumer-facing names have become harder to own with conviction. Even company-specific disappointments in areas like retail and EVs have been punished more sharply, which is another sign that market tolerance for weaker guidance is fading.

From a technical perspective, this is now a much more important test. The S&P 500 is no longer simply consolidating near prior highs. It is trading much closer to key moving-average support, and momentum has clearly weakened. I remain in the market-neutral camp here because the long-term trend is still intact, but the short-term setup has become more vulnerable.

Interest rates remain a central risk, especially with the 10-year Treasury yield continuing to swing in a wide range between roughly 3.6% and 4.35%. If yields stay elevated while unemployment indicators continue to tick higher, the market could struggle to regain clean upside traction in the near term.

My broader view remains that the SPY can still rally toward the 700 to 720 area over time if inflation stabilizes, yields calm down, and the geopolitical risk premium fades. But in the shorter term, support in the 620 to 650 range now matters much more.

That is the area investors should be watching as the next major floor over the coming months. As long as that zone holds, the longer-term uptrend remains structurally intact. But if oil stays elevated, rates remain sticky, and economic softness becomes more visible, the market is likely to remain choppy, rotational, and increasingly selective.

Overall, this week has been a reminder that the market is no longer trading in a liquidity-driven environment where broad exposure solves everything. Geopolitical shocks, oil volatility, stubborn inflation risk, and a less forgiving rate backdrop are all forcing investors to focus more on balance sheets, earnings durability, and price discipline.

The long?term bull structure remains intact, but momentum has undeniably cooled. Until the macro backdrop turns more supportive, a neutral and selective posture continues to be the most rational approach. This market rewards discipline over impulse, quality over speculation, and patience over prediction. We’re shifting from a liquidity?driven surge to a fundamentals?driven grind. The broader trend is still constructive, yet the short?term tape demands respect, restraint, and tactical flexibility.

That’s exactly where RoboInvestor delivers an edge. Designed for a choppy, headline?sensitive environment, our AI?powered advisory zeroes in on statistically grounded setups with clearly defined risk?reward. It keeps you engaged without drifting into overtrading, helping you act with precision rather than react to noise.

Every other weekend, you’ll receive the RoboInvestor newsletter—a concise, high-signal read with market context, technical outlooks, updates on open positions, and clear, actionable trade ideas. Hence, you’re prepared and confident heading into Monday’s open.

Explore our latest forecasts, trade signals, and live strategy sessions at Tradespoon.com. Navigate uncertainty with confidence—and position yourself ahead of the curve.

Whether you’re targeting blue-chip stocks, ETFs, commodities, or inverse ETFs, RoboInvestor offers a flexible, forward-looking approach tailored to today’s market conditions. Our model portfolio typically holds 12 to 25 carefully selected positions, and we’ve recently adopted an even more selective strategy—focused on quality, resilience, and opportunity.

Join us and take advantage of advanced AI technology to guide your investments with precision and confidence.

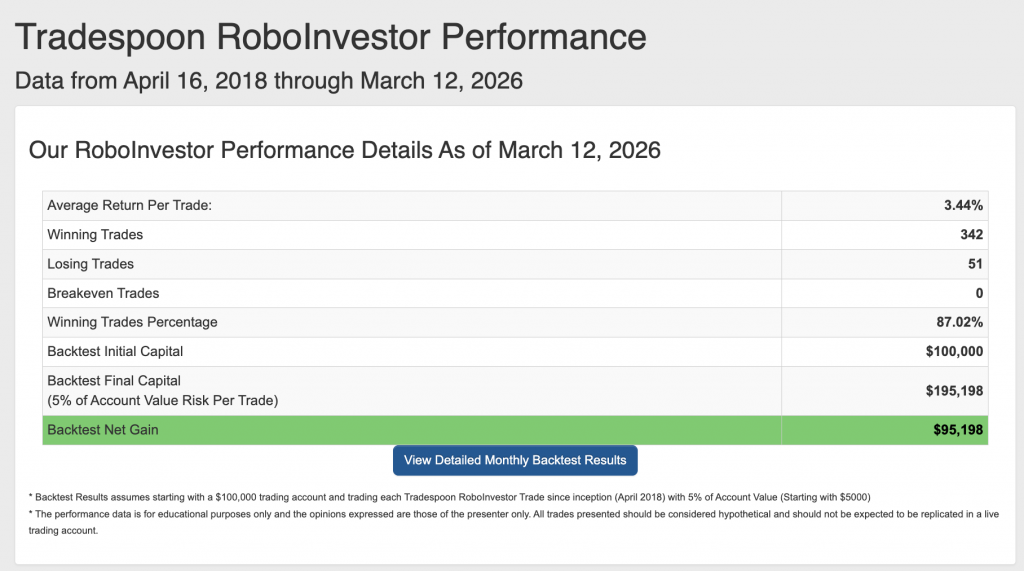

Our track record is one of the best in the retail advisory industry, with a Winning Trades Percentage of 87.02% since April 2018.

As we move toward Q2 2026 and geopolitical headlines continue to dominate the narrative, investors are navigating a market that appears stable on the surface yet increasingly selective beneath it. Tariff concerns briefly weighed on sentiment before easing, megacap earnings drew a sharper line between winners and laggards, and the Fed’s trajectory has grown less forgiving as inflation expectations stay stubborn. Interest rates have shifted from background noise to a defining variable, labor?market signals are softening at the edges, and market leadership is narrowing as investors demand a more direct link between spending, margins, and profits.

Volatility remains contained but reactive, quick to spike around policy shifts, earnings surprises, and moves in the bond market. In this environment, earnings quality and forward guidance are doing the real work of setting direction. Navigating the first quarter will require a disciplined, insight-driven approach that respects the influence of rates, manages employment risk, and stays flexible enough to participate in rotation without chasing fragile momentum.

Whether you are a seasoned investor or just starting, our team is here to help you every step of the way. Don’t face the challenges of tomorrow alone–join RoboInvestor today and take your investing to the next level.

Stay alert, stay strategic—and trade smart.

And remember, we’re not talking about day trading here. I’m looking for 50-100% gains within the next 3 months, so my weekly updates are timely enough for you to act.

*Please note: RoboStreet is part of your free subscription service. It is not included in any paid Tradespoon subscription service. Vlad Karpel only trades his own personal money for paid subscription services. If you are a paid subscriber, please review your Premium Member Picks, ActiveTrader, MonthlyTrader, or RoboInvestor recommendations. If you are interested in receiving Vlad’s personal picks, please click here.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!