Special Offer: Try the 'Tradespoon LIVE Membership' for ONLY $37!

CLICK HERE TO LEARN MORE

Special Offer: Try the 'Tradespoon LIVE Membership' for ONLY $37!

CLICK HERE TO LEARN MORE

Stocks have bounced on moments of diplomatic hope, but the bigger picture remains far less convincing. This week has been driven by war headlines, oil shocks, rising yields, sticky inflation risk, and a Federal Reserve that still looks stuck in wait-and-see mode, leaving the market vulnerable beneath the surface.

Stocks tried to stabilize this week, but the bigger picture remained far less convincing than a few rebound sessions might suggest. Under the surface, the market kept wrestling with the same difficult mix of forces: war in Iran, disruption around the Strait of Hormuz, elevated oil prices, tariff uncertainty, selective earnings reactions, sticky inflation risk, volatile Treasury yields, and a Federal Reserve that still does not have the flexibility many investors were hoping for. The result has been a market that can bounce sharply on temporary relief, yet still feels fragile underneath.

And remember, we’re not talking about day trading here. I’m looking for 50-100% gains within the next 3 months, so my weekly updates are timely enough for you to act.

Monday captured that tension perfectly. Global stocks rebounded from a four-month low after President Trump said he would postpone strikes against Iranian energy infrastructure and suggested talks were underway. Oil plunged more than 13% at one point, small caps outperformed, and investors treated the move as a badly needed release valve after the prior week’s pressure. But even then, the rally looked more like relief than resolution, especially because Iranian media quickly disputed the negotiation story. A market rising because one pressure point has temporarily eased is very different from a market rising because the macro backdrop has genuinely improved. This week was much more about the first category.

By Tuesday, that became obvious. Wall Street lost ground again as investors swung between hopes for diplomacy and fears that the conflict could drag on. Oil reversed higher, crude futures settled up more than 4%, and Treasury yields rose after a weak 2-year auction, reviving the market’s anxiety about a higher-for-longer setup in both energy and interest rates. At the same time, fresh business surveys showed the economic drag was no longer theoretical. Reuters reported that the flash U.S. Composite PMI fell to 51.4, its lowest level since last April, as higher energy costs weakened sentiment and pushed inflation fears higher. That is exactly the kind of backdrop that starts ringing stagflation alarm bells.

Wednesday brought another rebound, but again it was a conditional one. Stocks rose as oil fell and investors latched onto headlines that Iran was reviewing a U.S. ceasefire proposal. The market badly wanted to believe that a de-escalation path was forming, and that hope was enough to support risk appetite for a day. But this still did not feel like a clean macro reset. It felt like traders taking advantage of lower oil and softer fear, not like investors suddenly becoming confident that inflation, growth, and Fed risk had all been solved.

Thursday reminded everyone why this market still feels unstable. Hopes for a quick diplomatic resolution faded after a senior Iranian official called the U.S. proposal “one-sided and unfair,” while Iran also denied that talks were underway. Brent climbed above $105, global bond markets sold off, and Wall Street turned sharply lower again. By mid-afternoon, the Dow was down roughly 429 points, the S&P 500 had dropped 1.5%, and the Nasdaq had fallen more than 2%, leaving it more than 10% below its October 29 closing high and on track to confirm a correction. Energy was the strongest sector while technology and communication services were among the weakest, which tells you this market is still being driven less by earnings optimism and more by oil, inflation, and geopolitical fear.

That is also why the Federal Reserve remains central to the story. The Fed held rates last week at 3.50% to 3.75%, and officials have kept signaling that inflation risk remains the priority. On Thursday, a Reuters poll showed most economists still expect at least one cut later this year, likely around September, but markets have already priced out any easing this year and even built in roughly a 30% chance of a hike because crude has surged more than 40% since the conflict began. That disconnect matters. It tells you investors no longer believe a softer growth backdrop automatically means a supportive Fed. If oil stays high and inflation remains sticky, the central bank’s room to help becomes much narrower.

The broader macro warning signs are getting harder to ignore as well. The OECD said Thursday that the Iran war has erased what had been shaping up as a stronger global growth outlook. It now sees global GDP growth slowing to 2.9% in 2026, G20 inflation rising to 4.0%, and U.S. headline inflation reaching 4.2%. It also warned that while some tariff rates have come down after legal changes, the overall effective U.S. tariff rate is still well above where it stood before 2025. In other words, the market is not just dealing with war and oil. It is also dealing with an inflation-sensitive trade backdrop that still has not fully gone away.

The labor market has not broken, but it is no longer giving investors an easy all-clear either. Weekly jobless claims edged up to 210,000, which still points to relatively low layoffs, yet economists continue to describe the labor market as low-hire and low-fire. That kind of environment can hold up for a while, but it is vulnerable if higher energy prices, tighter financial conditions, and slower demand keep building. Housing is already feeling that pressure. Reuters reported that the average 30-year fixed mortgage rate rose to 6.38%, a six-month high, as oil-driven inflation fears pushed Treasury yields upward. That adds another layer of friction to an economy that was already losing some momentum.

Under the surface, sector rotation told the same story all week. Energy remained one of the clearest winners because higher crude prices kept pushing money into oil-linked names. Defense also stayed in focus as investors positioned for the possibility of prolonged conflict and higher military spending. Meanwhile, many fuel-sensitive and consumer-facing groups looked far more exposed. Carnival was a good example of that pressure. Reuters reported earlier this month that a 10% change in fuel cost per metric ton would reduce Carnival’s 2026 net income by $145 million, making it more exposed than major cruise rivals. With Carnival set to report first-quarter earnings on Friday, investors have had another reason to stay cautious on travel and leisure names that cannot easily outrun fuel risk.

Technology remained one of the most important battlegrounds, but even there the message was more selective than bullish. Nvidia stayed central to sentiment, and AI enthusiasm never fully disappeared, yet this has clearly become a show-me market. Micron illustrated that perfectly. Even after another strong AI-fueled earnings report, the stock slipped because investors focused on its plan to increase fiscal 2026 capital spending by $5 billion to more than $25 billion. That is one of the clearest signs that we are no longer in an easy momentum environment. Good stories still matter, but now they have to survive much tougher scrutiny around margins, capex, and durability. At the same time, company-specific bright spots still showed up in pockets of the tape, with Chewy jumping midweek after upbeat guidance reassured investors that some consumer stories still have room to work in a difficult market.

There were also a few notable corporate headlines outside the macro storm. Reuters reported that Equitable and Corebridge announced a merger that would create a $22 billion insurance giant, a reminder that strategic dealmaking is still happening beneath the surface. But the fact that news like that barely changed the tone of the market tells you how dominant the war-oil-rates narrative has become. Right now, investors care much more about the next move in crude, the next comment out of Tehran or Washington, and the next shift in Fed expectations than they do about ordinary corporate activity.

My view remains market-neutral. Momentum has clearly deteriorated, and that matters more right now than the broad bullish narratives that carried the market earlier in the cycle. The long-term trend is not fully broken, and I still believe the SPY can eventually work its way toward the 680 to 700 area if inflation cools, yields calm down, and the geopolitical premium fades. But for now, the far more important question is whether support in the 620 to 650 zone can hold over the next few months. If it does, this can still be viewed as a difficult but manageable correction inside a broader uptrend. If it does not, then the market likely stays trapped in a more volatile, rotational, and selective regime where broad exposure does less of the work and stock picking matters much more.

That’s the real takeaway from this week. We’re no longer in a liquidity?fueled market where broad participation lifts nearly everything. This tape demands discipline, selectivity, and evidence. Buyers still appear when fear cools, but rallies struggle to extend because oil, inflation, rates, and growth keep tugging in different directions. Until that tension breaks, caution still deserves a seat at the table.

That’s exactly where RoboInvestor creates an edge. Built for a choppy, headline?driven environment, our AI?powered advisory focuses on statistically grounded setups with clearly defined risk and reward. It keeps you engaged without drifting into overtrading, helping you act with precision instead of reacting to noise.

Every other weekend, you’ll receive the RoboInvestor newsletter—a concise, high-signal read with market context, technical outlooks, updates on open positions, and clear, actionable trade ideas. Hence, you’re prepared and confident heading into Monday’s open.

Explore our latest forecasts, trade signals, and live strategy sessions at Tradespoon.com. Navigate uncertainty with confidence—and position yourself ahead of the curve.

Whether you’re targeting blue-chip stocks, ETFs, commodities, or inverse ETFs, RoboInvestor offers a flexible, forward-looking approach tailored to today’s market conditions. Our model portfolio typically holds 12 to 25 carefully selected positions, and we’ve recently adopted an even more selective strategy—focused on quality, resilience, and opportunity.

Join us and take advantage of advanced AI technology to guide your investments with precision and confidence.

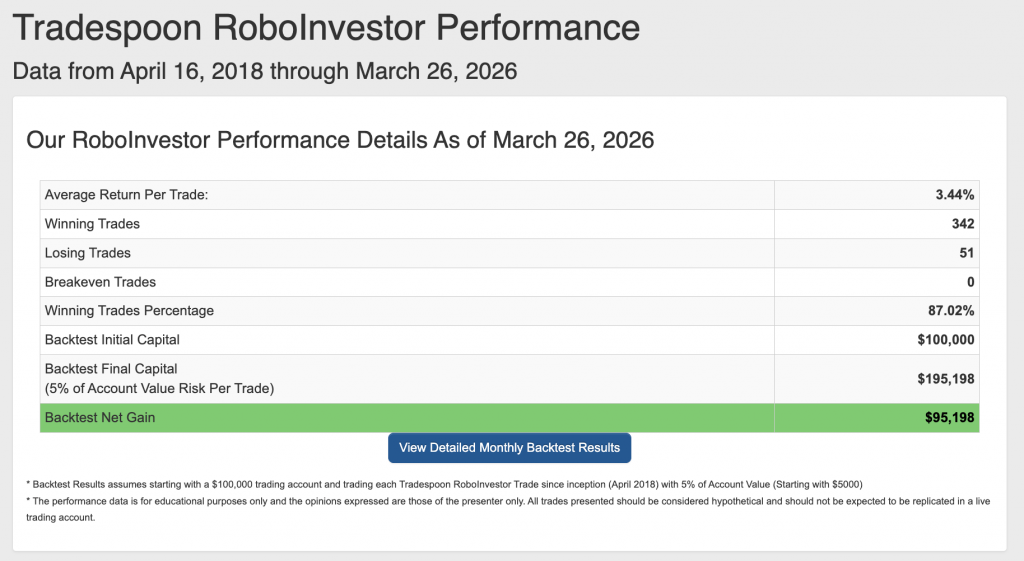

Our track record is one of the best in the retail advisory industry, with a Winning Trades Percentage of 87.02% since April 2018.

As we move into Q2 2026 and geopolitical headlines continue to dominate the narrative, investors are navigating a market that appears stable on the surface yet increasingly selective beneath it. Tariff concerns briefly weighed on sentiment before easing, megacap earnings drew a sharper line between winners and laggards, and the Fed’s trajectory has grown less forgiving as inflation expectations stay stubborn. Interest rates have shifted from background noise to a defining variable, labor-market signals are softening at the edges, and market leadership is narrowing as investors demand a more direct link between spending, margins, and profits.

Volatility remains contained but reactive, quick to spike around policy shifts, earnings surprises, and moves in the bond market. In this environment, earnings quality and forward guidance are doing the real work of setting direction. Navigating the first quarter will require a disciplined, insight-driven approach that respects the influence of rates, manages employment risk, and stays flexible enough to participate in rotation without chasing fragile momentum.

Whether you are a seasoned investor or just starting, our team is here to help you every step of the way. Don’t face the challenges of tomorrow alone–join RoboInvestor today and take your investing to the next level.

Stay alert, stay strategic—and trade smart.

And remember, we’re not talking about day trading here. I’m looking for 50-100% gains within the next 3 months, so my weekly updates are timely enough for you to act.

*Please note: RoboStreet is part of your free subscription service. It is not included in any paid Tradespoon subscription service. Vlad Karpel only trades his own personal money for paid subscription services. If you are a paid subscriber, please review your Premium Member Picks, ActiveTrader, MonthlyTrader, or RoboInvestor recommendations. If you are interested in receiving Vlad’s personal picks, please click here.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!