Special Offer: Get a 'Standalone' WeeklyTrader Membership for much less than the cost of the entire Elite Membership!

CLICK HERE TO LEARN MORE

Special Offer: Get a 'Standalone' WeeklyTrader Membership for much less than the cost of the entire Elite Membership!

CLICK HERE TO LEARN MORE

Stocks remain near record territory, but rising yields, tariff uncertainty, and a clear shift away from high-multiple growth are tightening conditions beneath the surface—setting up a data-heavy week that could determine whether this market consolidates constructively or slips into compression.

We are entering this week with markets still digesting last week’s crosscurrents.

The major indices closed the previous week mostly positive, but the leadership shift beneath the surface tells a more important story. Between February 14th and 17th, the S&P 500 and Dow Jones Industrial Average pushed to fresh all-time highs before momentum cooled. Large caps held up reasonably well into Friday’s close, yet the internal tone was more complex. Capital rotated out of higher-multiple technology names and into value-oriented and industrial exposure. The Nasdaq showed resilience at times, but during rate-driven sessions, it was clearly the relative laggard.

The labor market remains the central force driving this environment. January’s nonfarm payroll report, which continues to anchor pricing, showed 256,000 jobs added versus expectations closer to 180,000. Unemployment held at 4.1 percent, and wage growth remained firm at 0.4 percent month over month. That combination forced markets to recalibrate expectations for Federal Reserve policy. The probability of aggressive rate cuts in 2026 declined meaningfully, and near-term easing expectations were pushed further out.

The bond market responded decisively. The 10-year Treasury yield climbed during the repricing phase and continues to trade in a volatile but defined range between 3.6 and 4.35 percent. Each move toward the upper end of that range tightens financial conditions and pressures growth valuations. That explains why technology and AI-linked names saw sharper pullbacks during heavier sessions while financials and industrials quietly absorbed capital.

Trade policy added another layer of uncertainty into Friday’s close. The administration reaffirmed plans to move forward with tariffs on Canada, Mexico, and China, including 25 percent on steel and aluminum and 10 percent on additional Chinese goods. Even after legal challenges to certain emergency authorities, officials signaled they would pursue alternative routes to maintain the tariff agenda. Markets did not unravel, but cyclical sectors and small caps experienced intermittent weakness. The Russell 2000 lagged during risk-off windows, the dollar strengthened, and volatility spiked intraday before settling.

Earnings season reinforced how selective this market has become. Big technology and semiconductor names faced profit-taking after extended runs. Some cloud-exposed companies signaled moderation in capital expenditure growth, reviving concerns that surfaced late last year. Meanwhile, financials and industrials benefited from rotation, reflecting investor preference for durable cash flows in a higher real-yield environment.

Consumer data also contributed to the higher-for-longer narrative. Preliminary sentiment readings showed declining confidence alongside firmer inflation expectations. That combination pressures rate-sensitive sectors and supports the idea that the Fed has little urgency to ease.

Now, as we open Monday, February 23rd, the focus shifts from last week’s digestion to this week’s catalysts.

Markets are reacting to mixed macro signals. Treasury yields ticked higher ahead of key Federal Reserve communications, and traders are positioning for a dense economic calendar. Industrial production, capacity utilization, and housing data will provide insight into real economy momentum. Initial jobless claims and regional manufacturing surveys will further refine the labor and production picture.

The most important release later this week will be the Fed’s preferred inflation gauge, PCE. Alongside it, updated GDP figures, home sales data, and consumer sentiment will help determine whether growth remains firm enough to justify higher rates for longer. Several Fed officials are scheduled to speak, and tone will matter as much as the numbers themselves.

Corporate earnings continue to shape sector leadership. Reports from major retailers, semiconductor firms, and transportation companies will offer real-time insight into consumer demand, AI-related chip cycles, and logistics trends. In this tape, guidance matters more than headlines. Investors are rewarding durability and punishing even minor disappointments.

The dominant theme remains consistent. Higher real yields, tariff uncertainty, and digestion in large-cap growth are compressing multiples. At the same time, value exposure and economically sensitive sectors are providing relative stability. This is not broad-based risk aversion. It is disciplined rotation.

Technically, the longer-term structure of the market remains constructive. There is a credible path for SPY to work toward the 700 to 720 range in the coming months if earnings resilience persists and yields stabilize. However, near-term support between 650 and 660 remains critical. A sustained break below that zone would likely accelerate de-risking and volatility.

Momentum has cooled, which is why I remain in the market-neutral camp. The immediate threat is not a structural breakdown. The risk is compression. If rates stay elevated while unemployment indicators begin to edge higher, valuations come under pressure, and trading conditions become choppier.

As we begin this week, the message is straightforward. Do not chase strength at extended levels. Respect the bond market. Watch inflation data closely. In this phase, discipline and selectivity matter more than aggression.

This is a market to manage carefully, not one to react to impulsively.

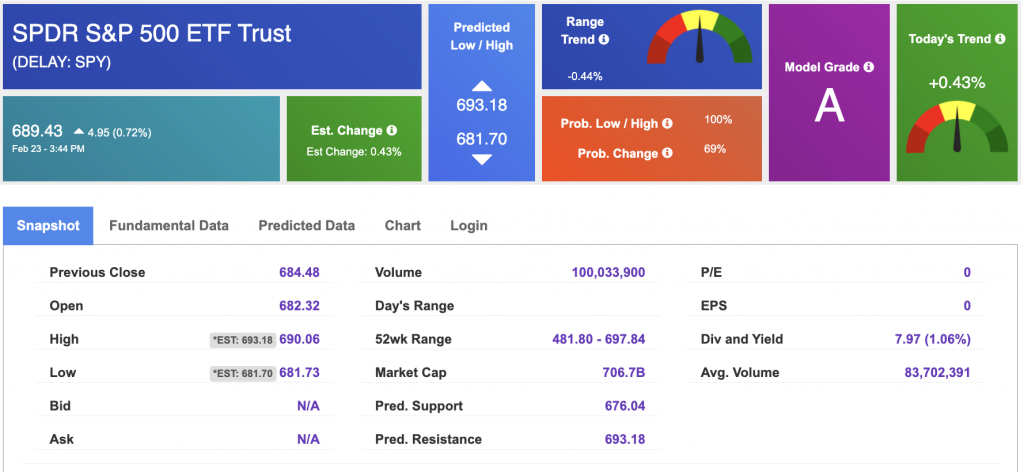

Using the “SPY” symbol to analyze the S&P 500, our 10-day prediction window shows a near-term positive outlook. Prediction data is uploaded after the market closes at 6 p.m. CST. Today’s data is based on market signals from the previous trading session.

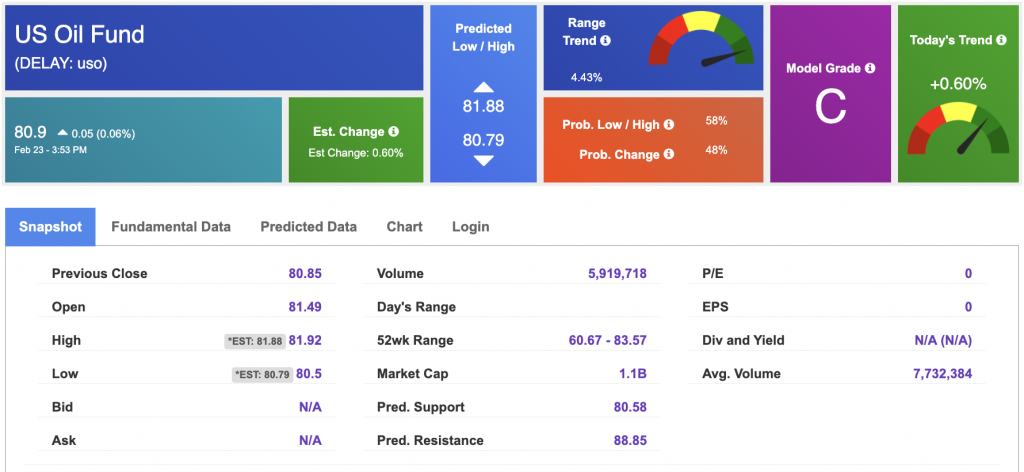

West Texas Intermediate for Crude Oil delivery (CL.1) is priced at $66.29 per barrel, down 0.29%, at the time of publication.

Looking at USO, a crude oil tracker, our 10-day prediction model shows mixed signals. The fund is trading at $80.9 at the time of publication. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

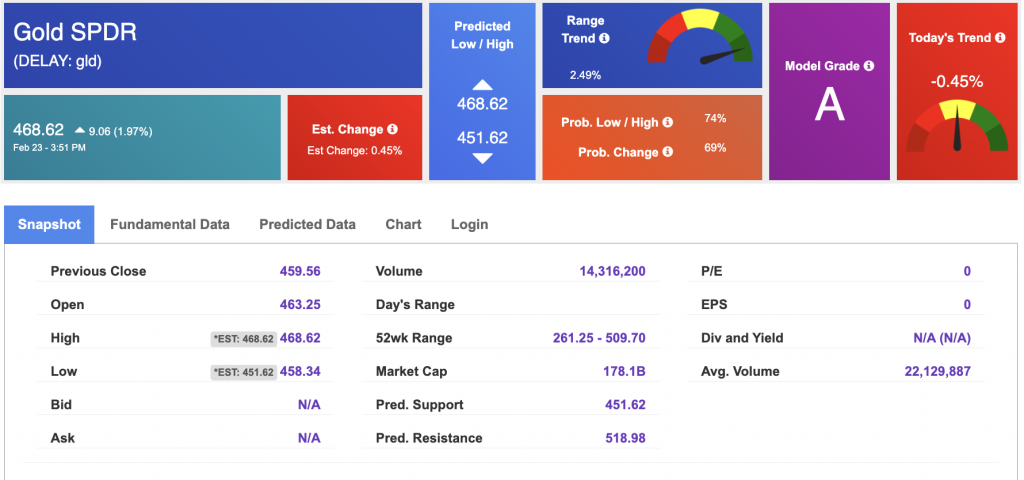

The price for the Gold Continuous Contract (GC00) is up 3.30% at $5,248.40 at the time of publication.

Using SPDR GOLD TRUST (GLD) as a tracker in our Stock Forecast Tool, the 10-day prediction window shows mixed signals. The gold proxy is trading at $468.62 at the time of publication. Vector signals show -0.45% for today. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

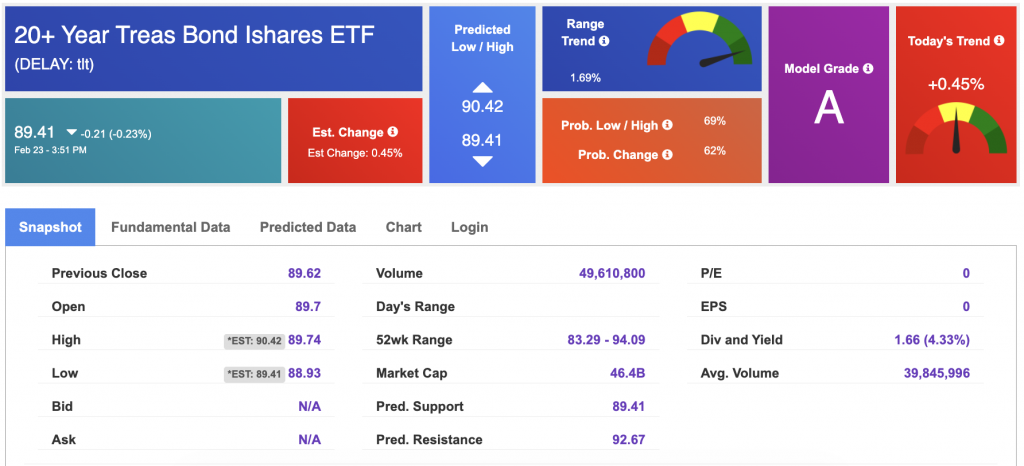

The yield on the 10-year Treasury note is down at 4.037% at the time of publication.

The yield on the 30-year Treasury note is up at 4.706% at the time of publication.

Using the iShares 20+ Year Treasury Bond ETF (TLT) as a proxy for bond prices in our Stock Forecast Tool, we see mixed signals in our 10-day prediction window. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

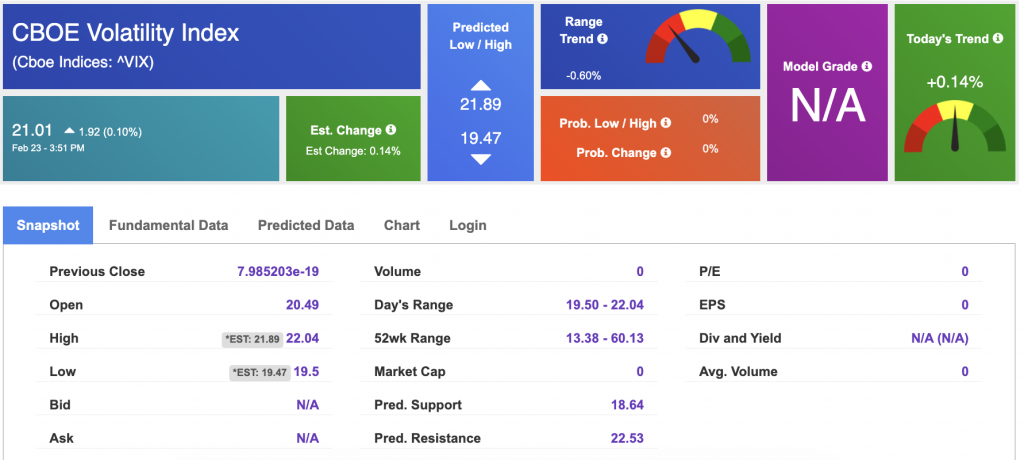

The CBOE Volatility Index (^VIX) is priced at $21.01 at the time of publication, and our 10-day prediction window shows mixed signals. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!