Limited Time Offer: Get Instant Access to the 'Elite' Trading Circle! (Monthly Plan Available)

CLICK HERE TO LEARN MORE

Limited Time Offer: Get Instant Access to the 'Elite' Trading Circle! (Monthly Plan Available)

CLICK HERE TO LEARN MORE

RoboStreet – Weekly Market News & Sentiment: Escalating Middle East Tensions Drive an Energy Spike and Reintroduce Inflation Risk, Labor Data Signals Emerging Economic Softness, Defensive Rotation Builds as Investors Reassess Risk, Volatility Returns to the Market Landscape, and Treasury Yields Keep Equities Trading Near Key Technical Levels

The first full week of March delivered a sharp reminder that markets rarely move in straight lines. What began as a fragile stabilization attempt near key technical levels quickly evolved into a far more complicated environment as geopolitical conflict, a surge in oil prices, and an unexpectedly weak labor report collided in real time.

Earlier in the week, markets were already grappling with rising Treasury yields and inflation-sensitive economic data. By Friday, those concerns were compounded by a sudden deterioration in employment conditions and escalating tensions in the Middle East, leaving investors reassessing both growth expectations and the Federal Reserve’s policy trajectory.

With the VIX hovering around 22 and major indices testing their 50-day moving averages, the market has shifted from steady momentum to a far more cautious and reactive posture.

U.S. equities entered Friday lower as geopolitical shocks and macroeconomic crosscurrents tightened financial conditions.

The S&P 500 declined roughly 2–2.4%, retreating from highs near 6,950 to close around 6,800–6,820. The Nasdaq Composite fell approximately 3–3.5%, reflecting the heightened sensitivity of growth stocks to rising interest rates and geopolitical uncertainty. Meanwhile, the Dow Jones Industrial Average proved relatively resilient, declining about 1.8–2%, supported by strength in energy and industrial sectors.

Technically, the market is now hovering around an important inflection point. The S&P 500 continues to trade near its 50-day moving average, a level closely watched by institutional investors as a gauge of whether the broader uptrend remains intact or begins to deteriorate.

Volatility also returned as a meaningful market force. The VIX briefly spiked above 25 midweek before settling near 22, indicating elevated caution but not outright panic. This type of volatility profile typically produces headline-driven trading and sharper intraday swings.

Meanwhile, the bond market remains the primary macro driver. The 10-year Treasury yield has continued to trade within a wide 3.6%–4.35% range, moving back above the 4% level earlier in the week. That movement reflects the market’s ongoing struggle to reconcile two opposing forces: persistent inflation risk and emerging signs of economic slowdown.

The most immediate catalyst for market volatility was the rapid escalation of geopolitical tensions involving Iran.

Over the weekend and into Monday, U.S. and Israeli strikes targeted Iranian military and nuclear-linked infrastructure, reportedly killing senior members of the Islamic Revolutionary Guard Corps. Iran responded with retaliatory actions across the region, and the conflict expanded into neighboring areas, raising concerns about broader regional instability.

The development with the most direct market impact was the disruption to the Strait of Hormuz, one of the world’s most critical energy shipping routes and responsible for roughly 20% of global oil transit. Shipping activity slowed dramatically, effectively constraining energy flows through the region.

Energy markets reacted immediately. Brent crude surged above $90 per barrel for the first time in two years, climbing more than 5% during the week. At one point, Brent reached approximately $90.11, while West Texas Intermediate posted an even sharper weekly gain of roughly 25%. Brent itself rose about 19% over the week, highlighting just how quickly energy markets repriced supply risk.

The situation was further complicated when Kuwait reduced oil production due to storage constraints after shipping disruptions from the Strait of Hormuz began backing up regional supply chains. The combination of supply uncertainty and geopolitical risk fueled speculation that oil prices could climb dramatically if disruptions persist, with some analysts warning that crude could potentially reach $150 per barrel under an extended supply shock scenario.

For equity markets, the significance of this move goes far beyond energy profits. Higher oil prices directly feed into inflation expectations, complicating the Federal Reserve’s already delicate policy balance.

This dynamic was evident in the bond market. Early in the week, Treasury yields rose rather than fell during geopolitical stress, an unusual signal that investors were more concerned about inflation than economic contraction.

Economic data reinforced those concerns. Earlier in the week, the ISM Manufacturing PMI showed continued expansion, but its prices-paid component surged sharply, marking the highest reading since mid-2022 and signaling renewed cost pressures across the industrial economy.

Then, late in the week, the narrative shifted again with the release of the February employment report.

The report revealed a surprising decline of 92,000 jobs, far below expectations for a gain of roughly 60,000. While several temporary factors contributed—including strikes in the healthcare sector, severe winter weather, and statistical revisions—the report also underscored a broader reality: hiring momentum across many industries has slowed significantly.

The unemployment rate ticked up to 4.4% from 4.3%, adding to concerns that the labor market may be gradually weakening after years of strength.

At the same time, average hourly earnings continued to rise, increasing 3.8% year-over-year, highlighting the complex challenge facing policymakers. Wage pressures remain present even as job creation slows.

Financial markets reacted quickly. Stocks moved lower following the report as investors weighed the possibility of a cooling labor market against persistent inflation risks.

The U.S. dollar also weakened, with the DXY index falling toward the 99 level, as traders began reassessing the likelihood of future Federal Reserve rate cuts.

Corporate earnings also added context to the economic backdrop. Companies such as Marvell Technology (MRVL) provided updates reflecting continued demand tied to artificial intelligence infrastructure. Meanwhile, retail earnings from Ross Stores (ROST) and Target (TGT) painted a more nuanced picture of consumer behavior, suggesting that while spending remains active, shoppers are becoming increasingly price sensitive.

Investor sentiment shifted notably during the week as markets were forced to process multiple competing narratives simultaneously.

On one side of the equation, rising oil prices and geopolitical escalation have reintroduced an inflation risk premium into global markets. On the other, the unexpected decline in payrolls suggests that the U.S. economy may be entering a slower phase of growth.

This combination has created a complicated environment for asset allocation. The market is no longer trading a simple narrative of economic expansion or recession risk. Instead, investors are navigating a landscape where inflation pressures, geopolitical uncertainty, and potential economic softening are unfolding simultaneously.

That dynamic has triggered a rotation beneath the surface of the market. Energy stocks have rallied sharply alongside the rise in crude prices, while defensive sectors such as utilities and consumer staples have seen renewed demand.

Meanwhile, growth stocks have traded unevenly as Treasury yields fluctuate. The Nasdaq’s intermittent resilience earlier in the week reflects the fact that investors have not abandoned technology leadership entirely, but the environment has become far more tactical.

At this point, I remain firmly in the market-neutral camp.

Momentum across the major indices has clearly weakened, and the market’s sensitivity to both geopolitical headlines and macro data underscores how fragile sentiment has become.

The biggest structural risk remains the “higher-for-longer” interest rate environment. If energy prices remain elevated due to Middle East tensions, inflation could reaccelerate at a time when labor markets are already showing signs of slowing. That combination would make it extremely difficult for the Federal Reserve to ease policy in the near term.

At the same time, the latest employment data suggests that unemployment indicators are beginning to tick higher, indicating that the lagged effects of restrictive monetary policy may finally be filtering through the economy.

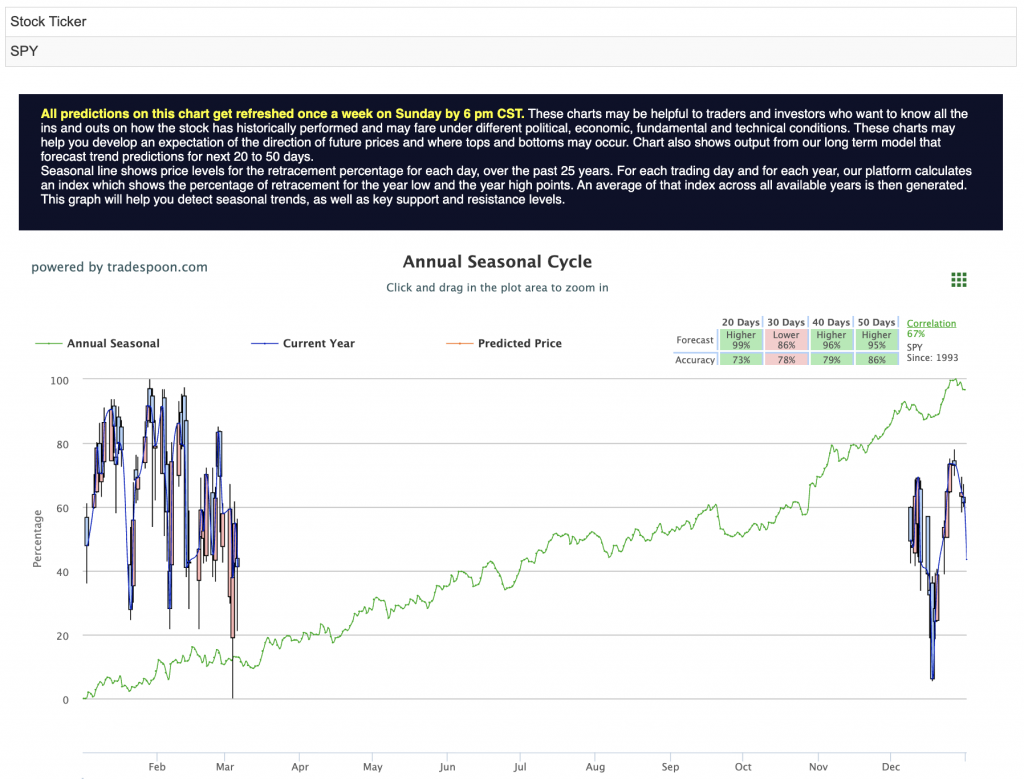

From a technical standpoint, the broader market structure remains constructive for now. The SPY still has the potential to extend its rally toward the $700–$720 range over the longer term, provided economic growth remains resilient and geopolitical tensions do not escalate significantly.

However, in the near term, maintaining support around the $650–$660 range will be critical. A sustained break below that zone could trigger a deeper correction as investors reduce exposure.

Looking ahead to next week, markets will turn their focus to a critical slate of inflation data, including the Consumer Price Index, Producer Price Index, and the Core PCE Price Index, the Federal Reserve’s preferred inflation gauge. These reports will likely play a major role in shaping expectations for monetary policy through the remainder of the year.

In addition, several major corporate earnings reports—including Oracle, Adobe, Ulta Beauty, and Dollar Tree—will offer further insight into technology spending, consumer resilience, and corporate pricing power.

Taken together, the market is now balancing three major forces at once: geopolitical risk, inflation dynamics, and emerging economic softness.

That combination will likely produce continued volatility in the weeks ahead. But for disciplined investors focused on long-term trends and strong fundamentals, periods like this often present the most meaningful opportunities.

That’s where RoboInvestor adds value. Built for a range-bound, headline-driven tape, our AI-powered advisory focuses on statistically grounded setups and defined risk-reward opportunities. It helps you stay engaged without overtrading and act with precision instead of reacting to noise.

Every other weekend, you’ll receive the RoboInvestor newsletter—a concise, high-signal read with market context, technical outlooks, updates on open positions, and clear, actionable trade ideas. Hence, you’re prepared and confident heading into Monday’s open.

Explore our latest forecasts, trade signals, and live strategy sessions at Tradespoon.com. Navigate uncertainty with confidence—and position yourself ahead of the curve.

Whether you’re targeting blue-chip stocks, ETFs, commodities, or inverse ETFs, RoboInvestor offers a flexible, forward-looking approach tailored to today’s market conditions. Our model portfolio typically holds 12 to 25 carefully selected positions, and we’ve recently adopted an even more selective strategy—focused on quality, resilience, and opportunity.

Join us and take advantage of advanced AI technology to guide your investments with precision and confidence.

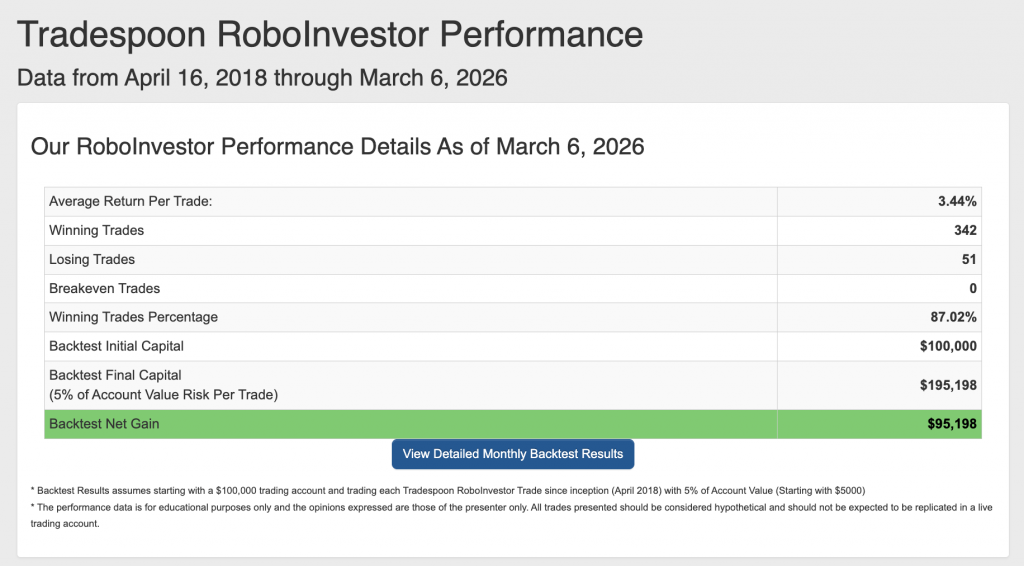

Our track record is one of the best in the retail advisory industry, with a Winning Trades Percentage of 87.02% since April 2018.

As 2026 gets underway, investors are stepping into a market that looks stable on the surface but is becoming more selective underneath. Tariff concerns briefly pressured sentiment before easing, megacap earnings exposed clear winners and losers, and the Fed’s path has grown less forgiving as inflation expectations remain sticky. Interest rates are no longer a background factor, labor-market signals are softening at the margins, and leadership is narrowing as investors demand a clearer connection between spending, margins, and profits.

Volatility remains contained but reactive, quick to spike around policy shifts, earnings surprises, and moves in the bond market. In this environment, earnings quality and forward guidance are doing the real work of setting direction. Navigating the first quarter will require a disciplined, insight-driven approach that respects the influence of rates, manages employment risk, and stays flexible enough to participate in rotation without chasing fragile momentum.

Whether you are a seasoned investor or just starting, our team is here to help you every step of the way. Don’t face the challenges of tomorrow alone–join RoboInvestor today and take your investing to the next level.

Stay alert, stay strategic—and trade smart.

And remember, we’re not talking about day trading here. I’m looking for 50-100% gains within the next 3 months, so my weekly updates are timely enough for you to act.

*Please note: RoboStreet is part of your free subscription service. It is not included in any paid Tradespoon subscription service. Vlad Karpel only trades his own personal money for paid subscription services. If you are a paid subscriber, please review your Premium Member Picks, ActiveTrader, MonthlyTrader, or RoboInvestor recommendations. If you are interested in receiving Vlad’s personal picks, please click here.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!