Special Offer: Try the 'RoboInvestor Membership' for ONLY $37!

CLICK HERE TO LEARN MORE

Special Offer: Try the 'RoboInvestor Membership' for ONLY $37!

CLICK HERE TO LEARN MORE

Stocks may be stabilizing, but the broader backdrop still looks unsettled. Between geopolitical tension, small-cap weakness, commodity pressure, and an uncertain Fed path, this remains a market where short-term relief can quickly give way to renewed volatility.

Stocks are trying to stabilize, but this still does not feel like a market that has fully regained its footing. Last Friday’s tone was shaped by a difficult mix of pressure points: escalating conflict involving Iran, disruption around key energy routes, elevated oil prices, tariff-related cost pressure, sticky inflation, firmer Treasury yields, and a Federal Reserve that still has very little room to sound truly supportive. That backdrop kept investors on edge and left the broader market looking vulnerable beneath the surface, even when short-term rebounds appeared.

Coming into this week, the tone has improved slightly, but mostly because the market is reacting to shifting headlines rather than a meaningful change in fundamentals. That distinction matters. This still feels like a tape where sentiment can swing sharply from optimism to caution in a matter of hours, depending on developments in geopolitics, energy prices, or interest-rate expectations. In other words, this is not yet a clean risk-on environment. It is a market attempting to recover while still carrying a heavy macro burden.

The geopolitical story remains one of the most important forces shaping investor behavior. Tensions involving Iran, the United States, and Israel are continuing to weigh on global sentiment, largely because markets understand the consequences of a prolonged disruption in energy. When oil becomes more volatile, it immediately feeds into inflation concerns, consumer stress, and uncertainty around Federal Reserve policy. Even when crude pulls back and stocks respond positively, that relief has not yet translated into real trust. Investors still know that this story can reprice the market very quickly, and that keeps volatility alive.

That helps explain why the recent bounce still feels fragile. The market is willing to react positively to any signs of de-escalation, but it has not fully moved past the idea that energy and inflation can reassert themselves at any moment. That has created a backdrop where every rally still feels somewhat conditional. Instead of investors confidently leaning into broad exposure, they are still asking whether the next geopolitical headline, oil move, or inflation surprise will interrupt momentum again.

The Federal Reserve remains another central piece of the puzzle. Policymakers are clearly aware that growth has softened in some areas, but inflation remains sticky enough to prevent a clean pivot. Recent commentary has reinforced a patient but cautious stance. There is growing acknowledgment that rate cuts may be possible later this year if the data allows for it, but nothing about the current setup suggests the Fed is ready to act aggressively. As long as inflation risks remain tied to commodities and geopolitical tension, the market is likely to keep treating monetary policy as uncertain rather than supportive.

That uncertainty is showing up in the market’s internal leadership. One of the clearest warning signs is small-cap weakness. The Russell 2000 slipping into correction territory is not just a technical headline. It reflects growing stress in the part of the market most exposed to tighter financial conditions, more expensive capital, and slower domestic growth. When smaller companies lag this badly, it usually suggests investors are becoming more selective and less confident in the broader economic backdrop.

Commodities are also sending a mixed but important message. Copper and gold both coming under pressure raises questions about global demand, economic momentum, and the market’s conviction in the growth outlook. Copper often acts as a barometer for industrial activity and economic confidence, so weakness there deserves attention. Gold pulling back alongside it adds another layer of complexity, because it suggests this is not simply a straightforward flight-to-safety or inflation hedge environment. Instead, investors appear to be reassessing multiple parts of the macro picture at once.

At the same time, there are still areas of emerging strength. One of the more notable themes is the growing mainstream acceptance of stablecoins and digital asset infrastructure. Stablecoins have quickly become a major part of the financial conversation, and the growth expectations around that space are drawing attention to crypto-linked platforms, payment rails, and blockchain ecosystems. That theme stands out because it offers one of the few pockets of clear structural momentum in a market otherwise dominated by caution and macro crosscurrents.

Technology remains a more selective story than it was earlier in the year. Investors are still willing to reward genuine earnings strength and real secular demand, but they are no longer handing out easy upside simply because a company is attached to AI, semiconductors, or growth. Stocks like Micron, Super Micro, and other high-profile movers are now being judged with a much harsher eye toward margins, spending, guidance, and execution. This is a major shift from the earlier momentum-driven phase of the market, and it reinforces the idea that this is now a more disciplined, more demanding environment.

There are also signs that parts of the real economy are stabilizing, which gives the market something constructive to work with. Manufacturing data has started to show modest improvement, and industrial activity appears to be firming after a prolonged soft patch. That does not erase concerns about inflation or geopolitics, but it does provide at least one counterbalance to the more negative narratives. If that stabilization continues, it could become an important support for sentiment in the weeks ahead.

This week’s economic calendar matters for exactly that reason. Consumer sentiment, manufacturing PMIs, jobless claims, and housing data will all help investors judge whether the economy is simply cooling or beginning to weaken more materially. That distinction is critical. If growth holds together while inflation gradually cools, the market has a path to stabilize. If inflation stays sticky while growth softens further, the environment becomes much more difficult, especially for rate-sensitive and lower-quality areas of the market.

My view remains market-neutral. Today’s tone is better than Friday’s, but not enough has changed to justify a more aggressive stance. This still feels like a selective, headline-sensitive, skill-based market where discipline matters more than chasing rebounds. There are opportunities, particularly in areas backed by durable growth or structural tailwinds, but broad conviction still looks premature. Small-cap weakness, commodity softness, geopolitical instability, and an uncertain Fed are all reminders that the surface action can look better than the underlying reality.

The biggest takeaway right now is that volatility is still the defining theme. Geopolitics, oil, inflation, and rates are continuing to pull against confidence, even as parts of the market try to recover. That does not mean the market cannot rally further from here. It means investors should be careful about mistaking a relief move for a true all-clear. Until oil settles, rate expectations become more stable, and growth data proves resilient enough to absorb these pressures, I think it makes sense to stay selective, stay flexible, and respect the fact that this market still feels stronger on the surface than it does underneath.

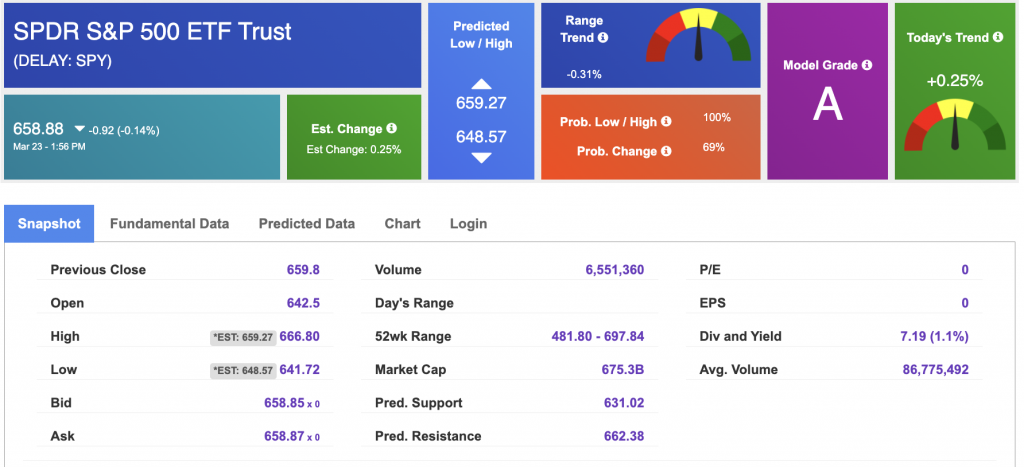

Using the “SPY” symbol to analyze the S&P 500, our 10-day prediction window shows a near-term positive outlook. Prediction data is uploaded after the market closes at 6 p.m. CST. Today’s data is based on market signals from the previous trading session.

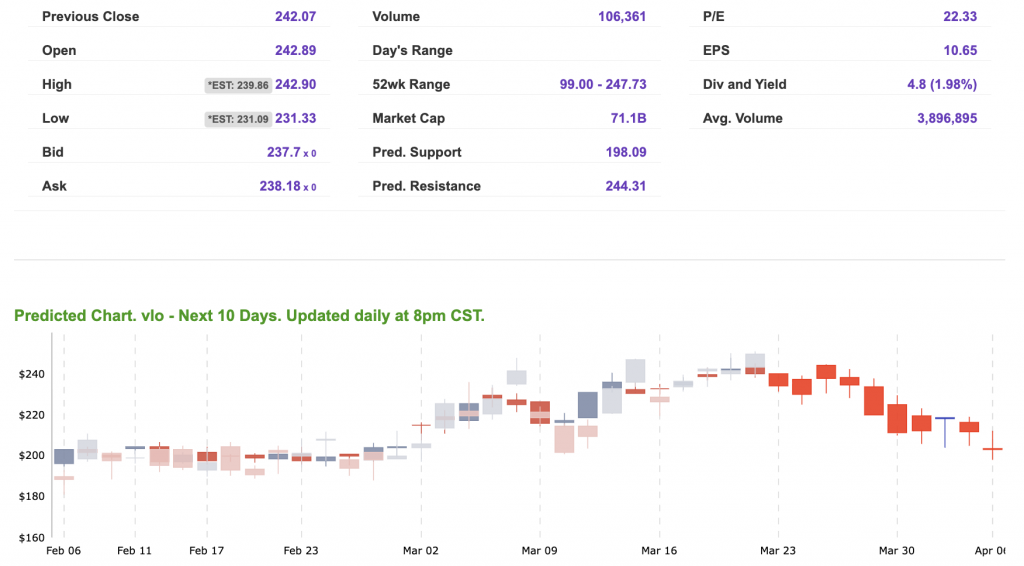

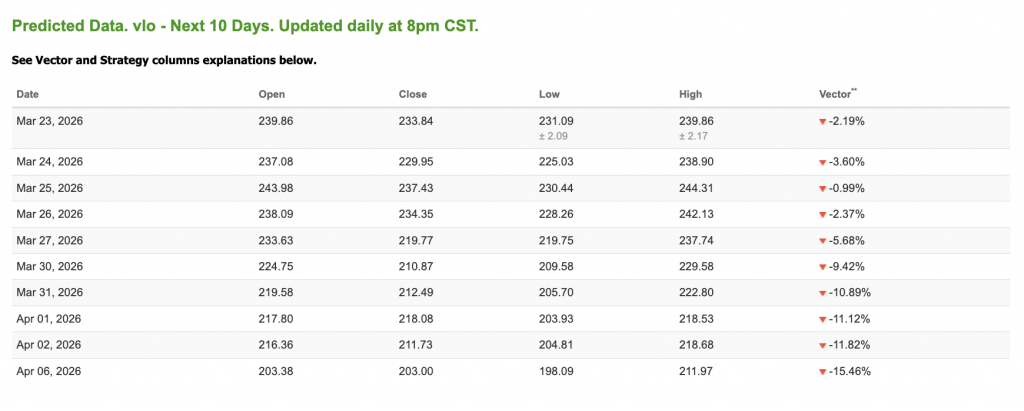

Our featured symbol for Tuesday is VLO. Valero Energy Corp. (VLO) is showing a steady vector in our Stock Forecast Toolbox’s 10-day forecast.

The symbol is trading at $327.81 with a vector of -2.19% at the time of publication.

10-Day Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Note: The Vector column calculates the change of the Forecasted Average Price for the next trading session relative to the average of actual prices for the last trading session. The column shows the expected average price movement “Up or Down”, in percent. Trend traders should trade along the predicted direction of the Vector. The higher the value of the Vector the higher its momentum.

*Please note: At the time of publication, Vlad Karpel does have a position in the featured symbol, vlo. Our featured symbol is part of your free subscription service. It is not included in any paid Tradespoon subscription service. Vlad Karpel only trades his money in paid subscription services. If you are a paid subscriber, please review your Premium Member Picks, ActiveTrader, or MonthlyTrader recommendations. If you are interested in receiving Vlad’s picks, please click here.

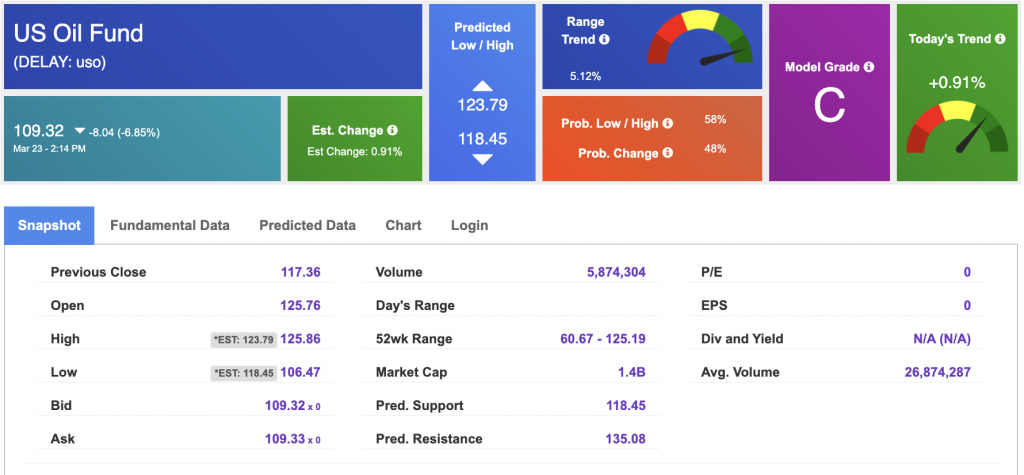

West Texas Intermediate for Crude Oil delivery (CL.1) is priced at $87.94 per barrel, down 10.52%, at the time of publication.

Looking at USO, a crude oil tracker, our 10-day prediction model shows mixed signals. The fund is trading at $109.32 at the time of publication. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

The price for the Gold Continuous Contract (GC00) is down 3.77% at $4,403.70 at the time of publication.

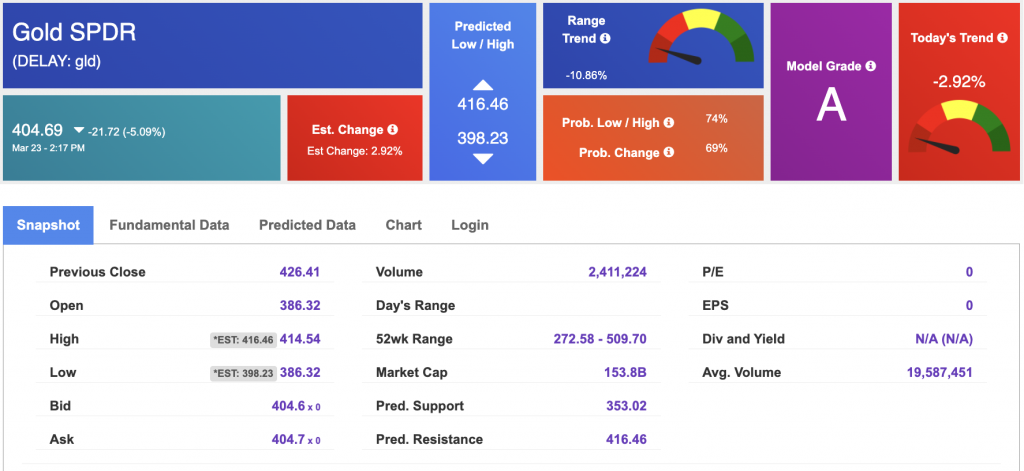

Using SPDR GOLD TRUST (GLD) as a tracker in our Stock Forecast Tool, the 10-day prediction window shows mixed signals. The gold proxy is trading at $404.69 at the time of publication. Vector signals show -2.92% for today. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

The yield on the 10-year Treasury note is down at 4.343% at the time of publication.

The yield on the 30-year Treasury note is down at 4.918% at the time of publication.

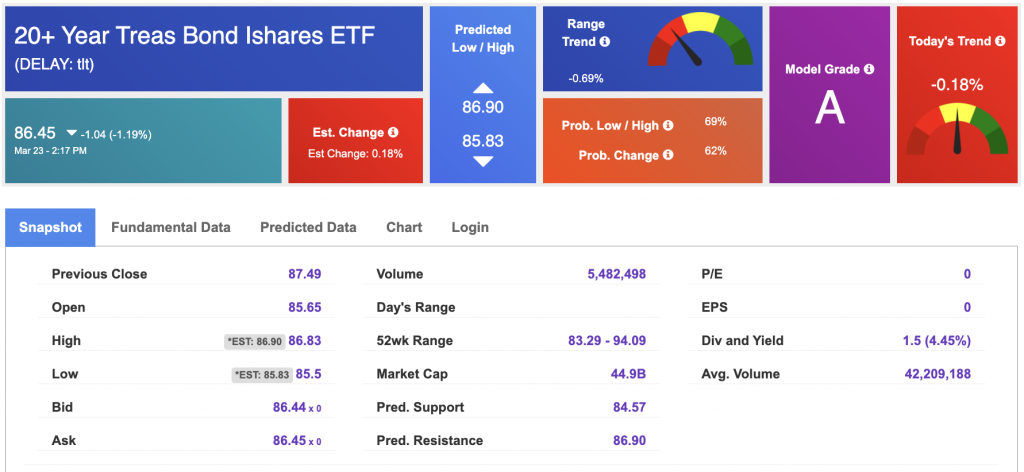

Using the iShares 20+ Year Treasury Bond ETF (TLT) as a proxy for bond prices in our Stock Forecast Tool, we see mixed signals in our 10-day prediction window. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

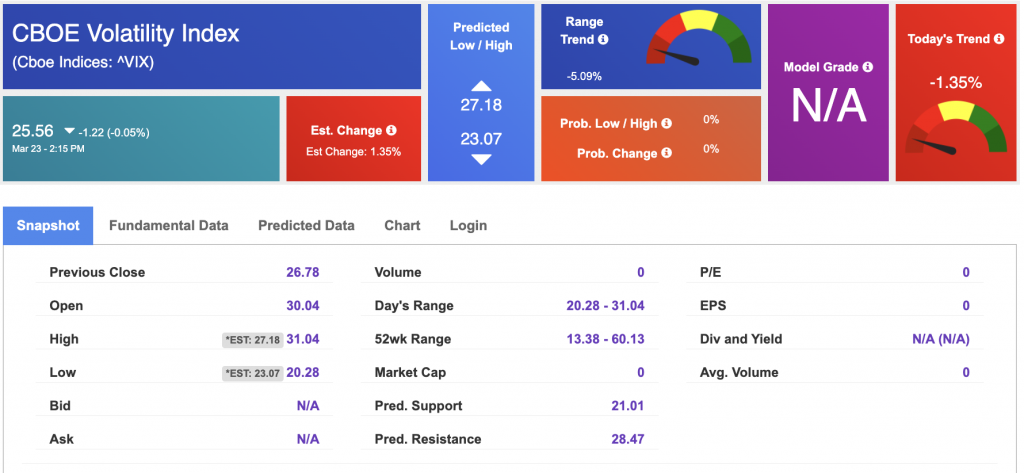

The CBOE Volatility Index (^VIX) is priced at $25.56 at the time of publication, and our 10-day prediction window shows mixed signals. Prediction data is uploaded after the market close at 6 p.m., CST. Today’s data is based on market signals from the previous trading session.

Please share this Tradespoon Market Commentary with your friends.

![]()

![]()

Comments Off on

Tradespoon Tools make finding winning trades in minute as easy as 1-2-3.

Our simple 3 step approach has resulted in an average return of almost 20% per trade!